Editor’s note: This paper was originally published at RalphVince.com in June 2014 and is reposed here with permission.

Repeatedly in both the gambling and trading communities the expected growth optimal fraction is employed, often referred to as the Kelly Criterion, and referring to the 1956 paper of John L. Kelly [2]. Though applicable in many gaming situations (though not all, blackjack being a prime example [15]) where the most that can be lost is the amount wagered, the Kelly Criterion solution is not directly applicable to trading situations which are more complicated.

Take for example a short sale. Clearly what can be lost is not the same as the price of the stock. Forex transactions incur a different analysis as one is long a currency specified in another currency (and thus vice-versa in effect, short that other currency against the long currency). Commodity futures represent a different problem than simply being long an equity in terms of a floor price (what, specifically, is the lowest, say, wheat can go? Clearly it has value and thus a price of zero may not be realistic, the risk on a long wheat futures transaction therefore actually less than the immediately priced contract amount), and they too are represented in a base currency. CD swaps, complicated strategies involving options, warrants, leaps, trades in volatility where the limiting function of zero as a price and maximum loss is distorted, interest rate products and derivatives all create a situation where the Kelly Criterion solution does not result in the expected growth-optimal fraction to risk, and, in fact, to do so is often to risk more than the actual expected growth-optimal fraction would call for [13]. Capital market situations. Given their inherent complexity, are not the same as gambling situations and the Kelly Criterion cannot be applied directly in determining proper expected growth-optimal fractions.

Further, as pointed out by Samuelson [8] (though he does not provide a computational solution), the Kelly Criterion solution (in those cases where it is applicable, i.e. wagering situations where what can be lost is equivalent to what is put up) seeks the asymptotic expected growth-optimal fraction as the number of trials approaches infinity. For example, in a single proposition where the probability-weighted expected outcome is greater than 0, the expected growth for a participant whose horizon is one trial is f = 1.0, or to risk his entire equity. If his horizon were longer (but necessarily finite) the expected growth optimal fraction would be greater than the Kelly Criterion solution but less than one. The handicapper who goes to the track for a ten-race card day, seeking to maximize his return for the day employs a horizon, Q, of ten. The portfolio manager, depending on his criteria, has a similarly finite number of periods. The Kelly Criterion solution (when applicable) is only an asymptote; it is never the expected growth-optimal fraction, but rather approached asymptotically as the number of trials approaches infinity. The Kelly Criterion solution, as well as closed-form formulations that seek to solve it, are asymptotic and always less than what is the actual, expected-growth optimal fraction.

As Hirashita [1] points out (referring to the asymptotic case), unless the payoff occurs immediately, the cost of assuming the risk is germane to the calculation of the expected growth-optimal fraction. Since we are discussing the finite case here, with a specific horizon, we must include the cost of the wager to the specific horizon as is expressed in our equation. Finally, the actual expected growth-optimal fraction formula should incorporate multiple, simultaneous propositions. The Kelly Criterion solution is therefore merely a subset of this more generalized formula, and represents only the asymptote to the special case where it is applicable.

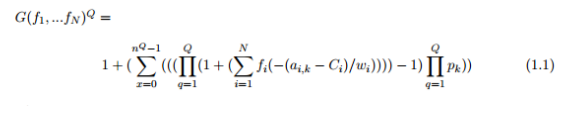

Presented here is the formulation for N multiple, simultaneous propositions at a horizon of Q trials, for all potential propositions. The solution is presented in the context of the N+1 dimensional leverage space manifold where for each of the N components, a surface bound between f{0,1} along each axis represents the fraction allocated to that individual proposition.

where:

Q = the horizon.

N = the number of components in the portfolio.

n = the number of possible outcomes in the outcomes copula.

k = int(x/(n(Q−q)))%n.

a N,n = the N x n matrix of outcomes in the outcomes copula.

pn = the n-lengthed vector of probabilities associated with each n in the outcomes copula.

wN = the worst case outcome of the all discrete outcomes associated with each of the N components.

Ci = the one period opportunity-cost of the risk in component i, per [13]. This is explained further, below.

Note k is a function of the iterators x and q, returning a specific zero’th-based row in the outcomes copula.

The drawdown constraint or other risk constraint as proposed in [11, 12] for a given Q can be employed upon the surface mapped by this equation in the leverage space manifold.

To compute the amount to allocate to replicate the percentage to allocation to a given individual proposition, i for a given fi:

Then for a given equity amount, the number of units to assume of component i to represent wagering fi percent:

The one period opportunity-cost of the risk in component i, used in (1.1) as Ci, is given in [13]:

where:

r = the current risk-free rate.

t = the percentage of a year for one period to transpire.

di = dividends, disbursements or costs (negative) associated over one period with one unit of the ith component

Si = the maximum of {f$i, regulatory (i.e. margin) requirement of the ith component}

where:

f$i = the amount to allocate to replicate the percentage to allocation to a given individual proposition, i for a given fi as given in (1.2)

We examine how to collect the data for determining the surface in leverage space at a given Q. Assume we have two separate propositions we wish to engage in simultaneously. For the sake of simplicity, suppose one is a coin toss paying 2:1, where we win with a probability of .5, and the other, a flawed coin paying 1:1 where we win with a probability of .6.

We create the copula to use as input from this data:

We note here that the number of components, N, is two since we have two separate, simultaneous propositions. The number of rows, n representing the space of what can happen for each discrete interval, is 4. w, the worst-case outcome for each N, each column, is −1 for both Coin 1 and Coin 2.

To see the equation graphically, consider that for the first interval, the possible outcomes are represented by the table. For the second interval, each node from the first interval now further branches by the number of rows in the table such that at a given period, q toward a horizon, Q, we have nq nodes. The formula can thus account for dependency by permitting the probabilities for the various rows in the copula to change at each subsequent interval based on the previous outcome(s) along a given branch being traversed.

The equation represents the surface in the leverage space manifold for given Q, f1, …fN. This surface represents what one would expect in terms of return, as a multiple on equity, after Q trials (hence, G(f1, …fN ) represents what one would expect in terms of a multiple on equity, on average, per trial). The maximum of this surface (i.e. the greatest G(f1, …fN ) Q or G(f1, …fN ), provides the expected growth-optimal fractions. The equation represents the actual (i.e. non-asymptotic) fractions to risk of N components (N >= 1) for all possible propositions; thus, all other expected growth-optimal solutions tend to be subsets of the asymptote (i.e. Q → ∞) of this more generalized equation, which is expressed here as

Equation (1.5) represents the asymptotic manifestation of equation (1.1). The proof of this is found in [14] and [4]. Since (1.1) yields the surface in the leverage space manifold after Q trials, (1.5) represents what this surface tends to asymptotically as Q → +∞. Since (1.5) is far less computationally expensive than (1.1) we can use (1.5) as a reasonable proxy of (1.1) after even a relatively small Q, thus for many calculations, including the expected risk-adjusted maximizing loci on this surface, ν and ζ as proposed in [4, 14, 15]as well as ψ proposed in [4] can be reasonably determined from (1.5).

References

[1] Y. Hirashita. Game Pricing and Double Sequence of Random Variables. Journal of Modern Mathematics Frontier, Vol.2 (2013),33-55.

[2] J. L. Kelly. A new interpretation of information rate. Bell System Technical Journal, 35:917–926, 1956.

[3] H. A. Latane. Criteria for choice among risky ventures. J. Political Economy, 52:75–81, 1959.

[4] M. L. de Prado, R. Vince and Q. J. Zhu. Optimal Risk Budgeting Under a Finite Investment Horizon SSRN, 2364092, 2013.

[5] L. C. MacLean, E. O. Thorp, and W. T. Ziemba(Eds.). The Kelly capital growth criterion: theory and practice. World Scientific, 2009.

[6] L. C. MacLean and W. T. Ziemba. The Kelly criterion: theory and practice. In S. A. Zenios and W. T. Ziemba, editors, Handbook of Asset and Liability Management Volume A: Theory and Methodology. North Holland, 2006.

[7] Edward O. Thorp and Sheen T. Kassouf. Beat the Market. Random House, New York, 1967.

[8] P. A. Samuelson. The fallacy of maximizing the geometric mean in long sequences of investing or gambling. Proceedings of the National Academy of Sciences of the United States of America 68: 2493-2496.

[9] R. Vince. Portfolio Management Formulas. John Wiley and Sons, New York, 1990.

[10] R. Vince. The New money Management: A Framework for Asset Allocation. John Wiley and Sons, New York, 1995.

[11] R. Vince. The Handbook of Portfolio Mathematics. John Wiley and Sons, Hoboken, NJ, 2007.

[12] R. Vince. The Leverage Space Trading Model. John Wiley and Sons, Hoboken, NJ, 2009.

[13] R. Vince. Risk-Opportunity Analysis. Createspace division of Amazon, 2012.

[14] R. Vince and Q. J. Zhu. Inflection point significance for the investment size. SSRN, 2230874, 2013.

[15] R. Vince and Q. J. Zhu. Optimal betting sizes for the game of blackjack. SSRN, 2324852, 2013.