Yield Curve

One of the core tenets of technical analysis that is taught by the CMT Association but that is often overlooked by many who are beginning their technical journey is intermarket analysis. We too often want to look solely at a price chart of an individual security and make our decisions. However, there is a robust well of information that exists either in economic data we may only analyze in the moment, or in asset classes that we tend to not pay attention to. As I have been fortunate in my career to work in equities, foreign exchange, commodities and fixed income, I understand the depth of information other asset markets can bring to the equation.

My approach at Stay Vigilant is to demystify the world of finance for the average investor. I call it demystifinance. I try to show how an institutional investor may consider fundamental, technical and catalyst information to make an informed decision. My hope is that you can as well. A major part of my work is intermarket and intertemporal analysis. This is what I will dig into this week.

The first chart today considers the yield curve. Many have heard that the yield curve predicts recessions. This is correct as the yield curve has a perfect hit rate. However, a big problem is that it has long and variable lags i.e. a recession could occur anywhere from 3 months to 2 years after it inverts. This may be why many were too negative in 2023. There is a logic as to why it should work as an inverted yield curve makes it less appealing for banks to lend money, which eventually slows the economy.

This first chart looks at three things – the 2 year vs. 10 year part of the yield curve with a horizontal line drawn at 0 to show where it inverts, the Bloomberg consensus economist odds of a recession in 6 months, and the yearly returns of the SPX. We can see three things: 1. A recession (red-shaded area) does occur after the curve goes below 0 2. The consensus economists only get this pessimistic right before a recession 3. SPX yearly returns are always negative once a recession happens. While none of this may be immediately actionable, it is an important backdrop to keep in our heads.

Correlation

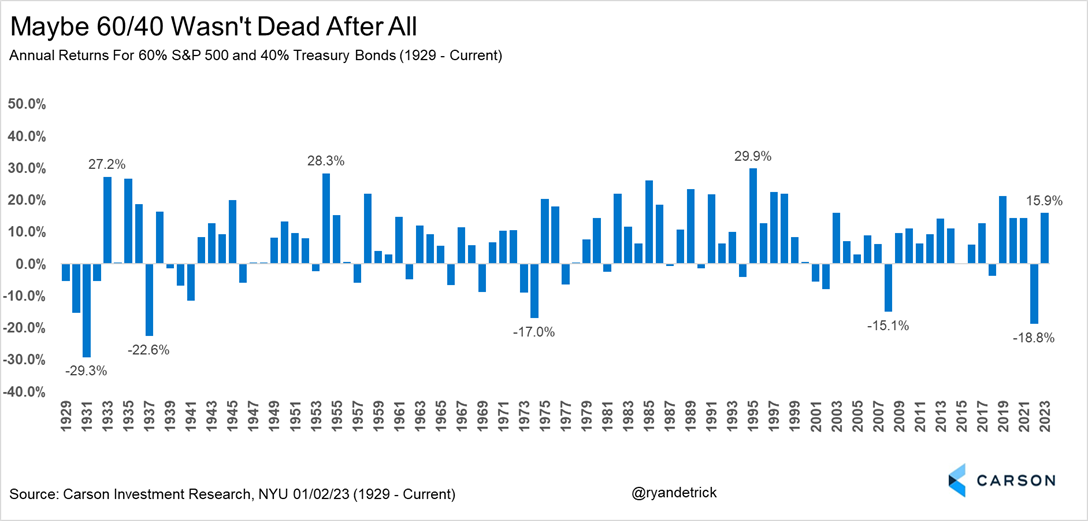

The most fundamental decision for investors, particularly at the start of the year, is whether (and how much) to allocate to stocks or to bonds. There are many approaches an advisor may take in helping a client reach this decision, but the fundamental premise is that the stability of fixed income can provide ballast to a sometimes volatile equity portfolio. As such, concepts such as the 60-40 portfolio for individual investors or risk parity for institutional investors have become quite common.

The second chart today looks at the correlation of stocks and bonds. For bonds, I use bond yields because I can get a longer time series of information. Remember, when bond yields go higher, bond prices go lower and vice versa. I look at the relative performance of stocks and bonds and compare it to inflation as measured by CPI. Inflation, after all, may have been THE story of 2023.

This chart shows that inflation is critical to the correlation of performance between stocks and bonds. On the right side of the chart, in the red box, I show that when inflation is low, stock returns and bond yields are positively correlated. This means stocks and bonds are negatively correlated. This is because the only concern is then growth, which means when stocks go higher on positive growth outlooks, bond yields (prices) go higher (lower) on expected higher rates. When stocks go lower on negative growth outlooks, bond yields go lower on expected Federal Reserve rate cuts. In both cases, stock prices and bond prices move in opposite directions meaning one hedges the other and provides a balanced portfolio.

However, on the left side of the chart, in the white box, we can see that in periods of high inflation/CPI, the opposite is true. Stock returns and bond yields are negatively correlated which means stock prices and bond prices are positively correlated. This is because the market is focused on inflation – higher inflation means higher yields expected and lower stock prices as inflation hurts margins. In these periods, the portfolio that consists of both stocks and bonds is not hedged as both assets move in the same direction. This is exactly what we saw on the negative side in 2022 and is what we have seen on the positive side in Q4 of 2023.

The question then remains for the investor: what is your view of inflation in 2024? Inflation will impact the move of stocks and bonds relative to one another.

Stocks vs. Bonds

Sticking with the stocks vs. bonds relative performance, I create an indicator from the ratio of the total return of the SPX Index and the US Treasury bond index. I compare this relative performance to economic indicators that get tracked and discussed in the market. After all, the economy leads earnings and earnings lead stocks. If the economy is doing well, all else equal, stocks should do well. If it is not doing well, stocks may struggle.

We saw in the first chart that both the yield curve and the consensus economists suggest there could be struggles in the economy sometime in the next 6 months. What about other indicators that may be more timely than these?

The first two you should consider in this chart are the US ISM Index (NAPM PMI) and the Leading Economic Indicators (LEI). Both of these are coincident with the stock market, which itself is a leading indicator. You can see that both of these headed lower for much of 2023 but have flat-lined a bit of late. As these stopped going lower, the relative performance of stocks vs. bonds has shot higher, perhaps much more than the economic indicators may suggest if history is a guide.

Two other economic data points I add on this chart are GDP (green) and the US unemployment rate (inverted in purple). I add these on the chart in order to show you that both of these data points lag the relative performance of stocks and bonds quite badly. While many in the news like to discuss these data points extensively, both are lagging as to the point of being almost useless for most market practitioners.

FOMC Rate Cuts

The final chart I want to show is the yearly performance of the SPX compared to when the FOMC cuts its discount rates. After all, if the economy has risk to it as some of the other charts suggest, that should mean the FOMC will cut rates. This should be good for stocks, right?

The market has been pricing in 6 rate cuts throughout 2024 even though the market broadly speaking is expecting a soft landing and not a recession. A soft landing is when the growth slows down but people don’t lose their jobs.

I look at 50 years of Federal Reserve Discount Rate and SPX yearly return data. I have drawn vertical white lines when the FOMC is cutting rates. The red-shaded area indicates when there is a recession. What you can see is that the FOMC has cut rates 8 times in these 50 years and there has been a recession 6 of these times. The other 2 times were what we would call a soft landing.

We can also see that if in fact we get a soft landing, the SPX yearly returns are positive. If we get a recession, the SPX returns are always negative. This would suggest the market returns right now are suggesting a soft landing with FOMC rate cuts forecast to occur. One finer point, however, the keen eye may see that the SPX yearly returns were negative in the period leading up to the rate cuts ahead of a soft landing. Thus, the market seems to have been responding more to no recession than actual rate cuts.

Restrictive Policy

Today I want to build on the concept of intermarket analysis, where we look at economic indicators, fundamental data and prices from other markets to help us assess the market that we invest in. We discussed the outlook for growth and inflation yesterday, and ended with the FOMC rate cuts and the economic soft landing being priced into the market.

The first chart today tries to anticipate why many in the market think the FOMC needs to cut rates in 2024. For this chart, I have created a custom index called ‘Restrictive’ which is simply the difference between CPI and the Federal Reserve Discount Rate. When this number is below zero, it means the Discount Rate is above the CPI and this policy may be deemed restrictive. When it is above zero, it means inflation is higher than the Discount Rate and the policy may be deemed easy. I compare this pink line to the yearly change in the SPX Index and the yearly change in GDP.

If we look at this pink line, when it has been below zero in the early 00s, around 2014-2015 and then in 2019, this restrictive policy has led to shrinking GDP and negative SPX returns. Right now, the policy by this measure would be deemed restrictive, yet we have seen neither negative SPX returns nor a shrinking GDP.

We can draw a parallel to the mid 1990s when this policy was also restrictive for quite some time but we saw neither negative growth nor negative equity returns. This is the soft landing period that we mentioned yesterday. This was a period of very strong global growth, particularly in emerging markets, that led to what Alan Greenspan referred to as a ‘savings conundrum’ with money flowing into the US from savers abroad. Perhaps this is what created easier financial conditions even though the policy was seen as restrictive.

Thus, investors today need to ask themselves if there are any exogenous factors that are making conditions easier today in the face of restrictive policy. This is what we may need to support economic and equity performance right now. Could it be an expansive fiscal policy? Could it be retiring Baby Boomers spending in the services economy? Could it be the development of AI?

Housing Market

One part of the US economy that is always a tried and true indicator of strength or weakness is the housing market. Given the large ‘multiplier’, housing stimulates economies by the large number of jobs created, the wide variety of products that need to go into a house, and the incremental of spending that results from orders for lumber, to copper for plumbing & electricity to the money spent at local diners by the workers. As a result, many people track housing as an important indicator of what may happen in the economy.

One critical data point that many investors follow is the National Association of Home Builders (NAHB) Index in white on the second chart. It is a composite index of strength or weakness in the economy and here I have inverted it so it lines up with the other data. It was strong in 2021, weak in 2022, started 2023 with a sharp bounce but has recently been struggling. What is leading to this?

The first suggestion would be mortgage rates. On this chart I use the average 30-year mortgage rate in the US in blue. We can see that it was historically low throughout the 2015-2021 period but moved sharply higher in 2022 and 2023. Federal Reserve rate hiking was a key driver to this but perhaps not the entire driver. I want to explore that because if the FOMC is set to cut rates, this could be a tailwind for housing.

The purple line is a custom index I created called mortgage spread (MORTSPD). It is the difference between the 30-year mortgage rate and 10-year US Treasury. I look at this spread because banks that provide mortgages will hedge their interest rate risk with the most liquid US Treasury which is the 10-year. Historically this spread averages between 1.5-2.0%. You can see that in 2023, this spread surge to 3.5%, the highest in 20 years. What happened? While we don’t know for sure, there are two things that I can think of that we may want to consider: 1. The Federal Reserve is shrinking its balance sheet which includes mortgage-backed securities 2. A banking crisis in March of 2023 has many banks unable or unwilling to make new loans. This is important as it may suggest some stickiness in how quickly mortgage rates will come lower even if the FOMC lowers rates.

The last line is another custom index that I created that I think does the best job of indicating the health of the housing market. Mortgage rates tell one piece of the story but as we all know, if mortgage rates are 0% and we do not have a job, we will not buy a house and take out a loan. Similarly, if mortgage rates are high, but we have a good job, we can afford those higher payments. My first mortgage was 8%. Thus, my custom index simply combines the 30-year mortgage rate and the US unemployment rate. You can see that this indicator did a better job of calling for strength in housing early last year when rates alone did not. It is still giving us a better signal, primarily because of the strength of the jobs market. This is another case where the soft landing (remember a slowdown with no job losses) is helpful to the economy and markets.

H.O.P.E.

A simple way that strategists have tried to capture this housing dynamic is in the acronym H.O.P.E. This stands for housing -> orders -> profits -> employment. The acronym covers how money/stimulus flows into and out of the economy. As lower rates make housing more appealing, the housing market picks up. This leads to a range of new orders for lumber, roofing, windows, copper and even furniture and landscaping. As companies start to process these new orders, they will start to generate profits. It is only after a company has been profitable for some time, that it starts to add workers and employment improves. This works in reverse too as a housing slowdown leads to a reduction in orders, declining profitability and then layoffs.

The third chart shows you visually this H.O.P.E. dynamic using the NAHB Index for housing, the ISM New Orders measure, S&P adjusted earnings per share and finally the yearly change in US labor force. As we look back through time, we can see that housing in white leads new orders in green. The next line to move is the profits in red and finally the employment in blue. The employment data is the most lagging of all of these, which is why I get less excited about it the first week of every month than everyone you may see in the media or politics.

Is the recent slowdown in housing a foreshadowing of tougher times ahead or was this just a blip in the data that will be reversed as mortgage rates come lower? This is a critical question that investors need to ask themselves.

XHB vs SPY

Finally, we can pull this together by looking at the performance of the housing ETF (XHB) and the S&P 500 (SPY). You can see that this ETF ever-so-slightly leads the SPY into and out of not only recessions but also bigger moves higher and lower in the market. It was the rally in XHB from the late fall 2022 into the early part of 2023 that presaged the move higher in SPY for the year. It was also the fall in XHB from August through October of 2023 that led to the move lower in stocks across the board. Since then, the XHB has rallied sharply coincident with the strong rally in all assets into the end of 2023.

Can this rally continue? This is the question that should be top of mind for investors as we start 2024. As goes housing, so goes the US economy and the broader US stock market.