Hello readers and welcome to another edition of Technically Speaking!

If sector rotations are the lifeblood of bull markets, then member engagement is the lifeblood of the association! The CMT Association built its foundation with the bricks of passion, perseverance, and most importantly, member participation.

As you may have noticed, the chart of member engagements is certainly picking up and moving to the higher left side, I’d say the trend is definitely bullish! But participation is not just limited to attending in-person events across the globe, although those are the best! Members and Affiliates can be a part of the association in multiple ways by contributing and sharing their research with the rest of the community. I’m going to be selfish here and list the newsletter as the first avenue of research contribution although there are multiple ways through Journal of Technical Analysis, Market Insights, Educational Webcasts, Investopedia partnership and many other local engagements. There’s just one small bridge that you’d need to cross to get to these fantastic avenues, and that is to reach out to us!

As we speak, members of the CMT Association are taking in the views of the sand dunes of Dubai at the CMT Summit Dubai 2024! And this is just the beginning. Member meetings are going to be more frequent and spread out, so that all of you can be a part of this growing community that we are building together!

I cannot stress enough on just how valuable these conversations and associations can be! You never know, maybe a dream opportunity could find you! I know it found me, so I’m not going anywhere! 😉

Hope to hear from a lot of you as we take the association to greater heights!

Until we meet again, think Technical!

Rashmi Bhatnagar

Editor

What's Inside...

President's Letter

By Robert Palladino, CMT

February has been an action-packed month for the CMT Association as we roll out two regional conferences across the world. The Board of Directors and the CMT staff both agreed...

I had the privilege of speaking with the legendary Robert Farrell at the CMT Association’s Midwinter Retreat in Tampa. He recommended I read a book called One-Way Pockets: the...

In yesterday’s missive, using the simple formula P=(F*V)S, I highlighted the inviolable link between long-term trends in both stock prices and fundamentals, and how all good things that happen to...

Interest Rates and Their Potential Impact on Equities

By Adam Turnquist, CMT

Key Takeaways:

The repricing of rate cuts further out on the calendar has pushed 10-year Treasury yields higher. Technically, the next major area of overhead resistance sets up at...

Cotton is forming a bull flag following last week’s breakout. Coffee futures are coiling below a critical polarity zone. Cattle and hogs are running wild. Even Dr.Copper is perking...

10-Year Treasury Rates: A Monthly/Secular Perspective Overview

By Stewart Taylor, CMT

I begin each year by reviewing the long-term technical positions and behaviors of what I think of as the “Big Four”—10-Year rates, S&P 500 ($SPX), Commodities, and the US Dollar....

CFA Institute Updates the Code of Ethics and Standards of Professional Conduct

By Stanley Dash, CMT

The CMT Association adopted the CFA Institute’s Code of Ethics and Standards of Professional Conduct (Code and Standards) in 2015. This replaced the MTA Code of Ethics that had been...

February has been an action-packed month for the CMT Association as we roll out two regional conferences across the world. The Board of Directors and the CMT staff both agreed at our Long-Range Planning meeting last August that we would focus our resources on delivering a series of regional conferences (globally) rather than a mega conference in New York City each year. The successful planning and execution of the 50th Annual Symposium in NYC last April was a monumental achievement, but we wanted to reach a wider audience in 2024 that may not have been able to make the trip to NYC.

The Mid-Winter Annual Retreat, held in Tampa on February 1st, provided over 100 attendees with a full day of presentations, interviews, trade idea discussion, and networking within our CMT community. The Association has had a full history dotted with mid-winter retreats ranging from Arizona to California to Florida; Tyler Wood and Bill Kelleher, who head up event planning, decided to rejuvenate that historical precedent by planning this event. I would like to personally thank Eric Caisse, who lives and works in Tampa and is a fellow Board member, for his effort in securing the event space and sponsorship dollars for the event. It is always enjoyable to see young technicians attend our events: we hosted a multitude of students from Florida Gulf Coast University under the stewardship of Ronald Mushock, CFA, their college professor, as they listened to Mark Dibble, Walter Deemer, Bob Farrell, and Craig Johnson among others present their lessons in technical analysis and risk management.

February has also kicked off the CMT’s Investment Challenge, which began on February 5th and will run until March 29th, with results being announced on April 5th. It is open to current CMT candidates and APP (Academic Partner Program) students. More than 525 candidates are registered for the Investment Challenge, and please keep track of results on the CMT’s LinkedIn page. If you need more information, please contact Kaizad Amrolia, Joel Pannikot, or Tyler Wood directly.

Lastly, the CMT Association is hosting an inaugural regional event in the Middle East region on February 28th and 29th. Dubai will be the location, and the Museum of the Future will be the venue. The Board of Directors and CMT Staff have been working on the logistics of this event for the last 6-8 months and I am sure it will not disappoint. There are nearly 200 registered attendees, speakers traveling from all over the globe, and the venue is second to none! After hosting such a fantastic event in NYC last April, I am beyond impressed that the CMT Association will be hosting its first event in what will hopefully become an extremely important strategic growth point for our Association. It is not too late to register if you are in the region!

I will be back in this space in March to discuss the results of the Dubai Symposium, several strategic growth focus points for the Association, and volunteer opportunities.

February has been an action-packed month for the CMT Association as we roll out two regional conferences across the world. The Board of Directors and the CMT staff both agreed at our Long-Range Planning meeting last August that we would focus our resources on delivering a series of regional conferences (globally) rather than a mega conference in New York City each year. The successful...

Author(s)

Robert Palladino, CMT

Robert Palladino, who holds a Chartered Market Technician (CMT) designation, is a senior foreign exchange trader for JPMorgan Chase with experience trading foreign exchange, commodities, and interest rate products, including…

I had the privilege of speaking with the legendary Robert Farrell at the CMT Association’s Midwinter Retreat in Tampa. He recommended I read a book called One-Way Pockets: the book of books on Wall Street speculation. Published in 1917, it was written by Don Guyon, the fictitious name of a man working in a brokerage house during the War Bride bull market of 1915. It is my hope to relay some timeless market wisdom, study some market history, and share a book recommendation from our first president.

History & Background

The year is 1915. Electricity, the internal combustion engine, running water in our homes, and the desire for city life over rural life are all changing the way we live. US equities have been in a secular trading range since 1900. We are in the midst of the War Bride bull market following the start of World War 1. See chart 1.

Chart 1

World War 1 officially started on July 28th, 1914. Trading on the New York Stock Exchange closed from July 30th to December 12th, 1914, as foreign investors began liquidating their holdings to raise money to fund the war. When trading resumed, The Dow Industrial average gained more than 86% over 257 trading days. This rally was fueled by the government as it began spending heavily to produce goods for the Europeans to purchase to support the war. The 1915 rally was led by the aptly named War Bride stocks, including munition, iron, steel, shipping, and textiles. See chart 2.

Don Guyon (DG), working in a brokerage house in December 1915, had a difficult time understanding why speculators were losing money at the end of such a spectacular bull run. To figure this out, he went through the accounts of six of the brokerage’s largest active traders. He analyzed their transactions from July 1st, 1915, to February 29th, 1916. See chart 2. He concluded, “…the trading methods of each [speculator] had undergone a pronounced and obviously unintentional change with the progress of the bull market from one stage to another”1

Chart 2

After doing his study by analyzing his brokerage’s order book, DG concluded that the speculators’ behavior was backwards. They were doing the exact opposite of what they should have.

When the bull market was in its infancy, DG found that speculators were taking quick, small profits and small losses. They were also using stop orders for protection.

As the bull market continued, they repurchased these stocks at higher prices. This time though, they took profits on larger gains than before. Some lost money by shorting in an attempt to call the top.

Even further into the bull market, speculators stopped taking any profits at all. They also stopped using protective stop orders, even as stocks doubled. The speculators did not want to be stopped out again.

They sold too soon, repurchased at higher prices, quit using stops, bought more stock after the market finally started distribution, and sold long positions on breaks lower instead of on rallies.

Before we get to DG’s trading methodology, he eventually offers the following regarding a speculator’s psychology. “The operating method I have outlined is not fool-proof or otherwise infallible… But the speculator who adhered closely to its rules may at least rest assured that his trading methods are diametrically opposed to the trading methods of the great majority of speculators – and the great majority of speculators are, as we know, consistent losers in Wall Street.”2

and

“The man who applies this or any other speculative method successfully must be able to exercise patience and self-control, to withstand all forms of mental temptation, to ignore the dictates of fear and greed, and to disregard everything he hears, sees, or reads that may cause the slightest deviation from his course.”3

and

“The few who make money in the stock market await what they consider exceptional opportunities and then play for profits that are worthwhile. They look ahead a week or a month or a year, as the case may be, and disregard the changes that occur in the price movement in each daily session, which to the daily trader assumes exaggerated proportions.”4

DG’s Plan to Speculate Covering a Complete Market Cycle

First determine the trend of the overall market, and then speculate in that direction. Be careful of rangebound markets, but if desired buy low and sell high.

How a bull market starts/when to get long:

Most speculators become convinced of a bull swing when it approaches its culmination.

Bull markets start after a protracted period of dullness and narrow fluctuations. Price breaks through the trading range with increased activity on the advances. Sometimes many stocks advance, while at other times the advance is narrow. Look for leaders entering new high territory as confirmation.

Bull markets might also begin after a period of declining prices when the market advances or refuses to go down on bad news. Look for when the market finally advances above the point where it was before the bad news as confirmation.

DG also tells us:

It is just as important to determine what to buy as when to buy. He recommends two or three active stocks, and he recommends buying stocks that have declined the least.

Write a trading plan before making any commitments. He reminds us that our judgement is most logical before having money in the market, which tends to warp ones sound judgement.

Use protective stop orders, and enter them at the same time as buy orders. Never lower or cancel them. Raise them in accordance with your predetermined plan. Set them based on market action/price. They should take you out of your positions when your idea is no longer valid, not based on an arbitrary number of points or a percentage.

Follow the plan. Do not change the plan because of news, market action, or any other outside influence based on things we hear, read, feel, etc…

Seeing the first reaction through:

You are now long. Your stocks have advanced for several days. DG tells us:

Do not make the mistake of trying to find the top and play for a reaction.

Do not sell, even if you are convinced the advance has gone too far too fast. This is the opposite advice of the cliche’, nobody ever goes broke taking a profit. He disagrees.

Stay invested as the issue pulls back 50% or more.

Add on strength when the price begins to resume its advance and the correction appears over. This second purchase should also have a protective stop.

The first selling point:

Your original line of long stock should be sold on the recovery to the former highs, while the stock bought on the reaction should be retained.

This process of buying shares on strength after pullbacks and selling shares at the previous swing highs should be repeated as long as the market continues to advance into new high territory.

Do not make purchases at new highs. “…this temptation is fatal alike to his mental attitude and the success of his operations.”5

The great distributive stage:

The market usually has several successive days in which the volume of sales is very large and speculative excitement is intense.

Stocks under distribution will have sharp but short-lived advances, followed by gradual declines.

There will come a time when, instead of resuming the advance, stocks will go sideways near their previous top. The action will look similar to the past and the public will again buy. This is the time to exit your position. Stock has been transferred from the strong hands to the weak hands.

Exit your position.

If this is happening at the broad market level, it is time to “get out of all stocks and stay out, regardless of the strength displayed by certain issues… Not only is this the time to sell long stock, it is also the time to put out a line of shorts.”6

When and what to sell short:

In contrast to buying stocks long, look to short the weakest issues. These are the ones breaking down from ranges well below their highs instead of at or near their highs.

Limit your losses using stops, just as you did on the long side.

Use the same tactics as longs, just in the opposite direction.

Remember, when selling short, rallies will be very, very sharp. Instead of covering too early, “cover your complete line only when the market no longer goes down on bad news or when it moves upward through a trading area…”7

Final Thoughts

DG’s perspective is a fascinating one. He studied actual buy and sell orders of unsuccessful speculators, and then he crafted trading guidelines which do the exact opposite of what they did. He shared important psychological ideas. He even made the case for Technical Analysis as a discipline: “To tell a speculator to base his operations on his interpretation of fundamental factors is to leave him just where he started…The market itself determines the relative importance of all factors more accurately.”8

I encourage you to read this book, and I again thank Mr. Farrell for this recommendation. In closing, DG tells us, and I believe Mr. Farrell would agree, “…the only speculative method that would prove profitable in the long run must be the reverse of that followed by the consistently unsuccessful public.”9

References

Guyon, Don. One-Way Pockets: the book of books on Wall Street speculation. New York, New York: Cosimo, 2005. Page 16.

Ibid. Page 63.

Ibid. Page 64.

Ibid. Page 62.

Ibid. Page 55.

Ibid. Page 54.

Ibid. Page 57.

Ibid. Pages 32-33.

Ibid. Page 7.

I had the privilege of speaking with the legendary Robert Farrell at the CMT Association’s Midwinter Retreat in Tampa. He recommended I read a book called One-Way Pockets: the book of books on Wall Street speculation. Published in 1917, it was written by Don Guyon, the fictitious name of a man working in a brokerage house during the War Bride bull market of...

Author(s)

Louis Spector, CMT

Louis Spector serves as the Curriculum Director for the CMT Association, where he led the rewrite and launch of the 2025 digital curriculum and continues to steward its ongoing development.…

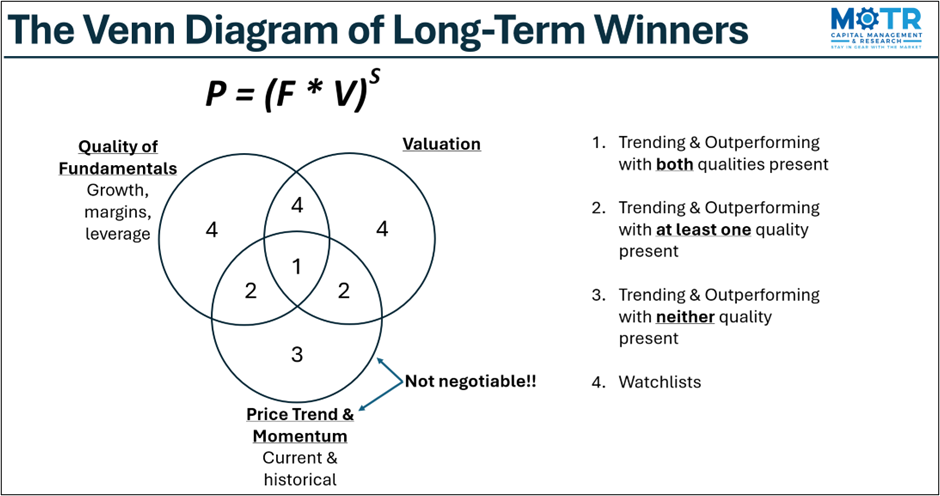

In yesterday’s missive, using the simple formula P=(F*V)S, I highlighted the inviolable link between long-term trends in both stock prices and fundamentals, and how all good things that happen to price begin with superior fundamentals, valuation expansion, and optimistic sentiment. “Multi-baggers” happen when price benefits from simultaneous improvements in all three of these inputs. However, I also drew a fine line yesterday between fundamentals and opinions of fundamentals, and how, in my view, the only opinion that matters is that of the market, or price trend itself.

Why is that? Because no matter what one thinks about a company’s future growth prospects and present valuation, that opinion will never be monetized favorably until the market agrees with it, via a strong price trend and relative outperformance.

In accordance with this philosophy then, investors should populate their portfolios with stocks that meet as many of these “multi-bagger” criteria as possible. The Venn diagram of long-term winners featured below provides a simple framework for thinking about this objective. Ideally, a portfolio will be full of “1s”, a smattering of “2s”, and perhaps a few “3s”. Most importantly however, “4s” should be avoided at all costs.

Some investors gain the greatest comfort from being contrarian, buying stocks when they are outside of the “Price Trend & Momentum” circle (i.e., “4s”). Of course, this might work out from time to time, but one of the few guarantees in this business is that no stock will everbe a multi-bagger without first making its way back into this circle. Let’s therefore call it the “Winner’s Circle”.

One can lean on this concept to assess the future prospects of an ETF, for instance. By mapping the holdings of an ETF to this Venn diagram of long-term winners, we can qualify whether or not the portfolio is positioned for future success.

By way of example, the ARK Innovation ETF (ARKK) chart pattern (below) would likely be identified by most technicians as a complex head & shoulders bottom, and I would agree. Another rotation higher, with a close above $55 would open the door to a run to the pattern’s upside target in the $95-$100 area (green box), which also overlaps with the Q1’21 lows, as well as the zone between a 50% and 62% retracement of the roughly -80% decline from 2022-2023.

Like the S&P itself, this ETF can only achieve that objective if the stocks within it are up for the challenge. In the” P=F*V” framework (inset in chart above), we can see that the average (Avg) trend score (TR) and momentum score (MO) hover just above average at 54 and 58, respectively.

In terms of fundamentals (F), using data from Koyfin.com, we can simply calculate the growth quality (GQ) and returns quality (RQ) of each stock compared to the rest of the market. Befitting the manager’s style, we can see that the average stock’s GQ score is far greater than its current RQ score (73 & 34, respectively). This suggests that the manager’s expectation is that these stocks, on average, will grow themselves into profitability, a characteristic mindset of those investors trafficking in the disruptive technology space.

Finally, we have valuation (V). Here, we can see that the average stock in the portfolio scores rather poorly from a valuation (VA) perspective relative to the rest of the market (14). This too is almost par for the course for hyper growth investors, banking that stocks that look expensive today are likely to look cheap in hindsight once the expected growth and profitability come through. In history, Amazon was a good example of this, where famed value investor Bill Miller was ridiculed and chastised for owning Amazon in the Legg Mason Value Fund. He pushed back saying it was inexpensive based on future growth, and boy was he ever proven right!

Just as the price-earnings ratio (PE) is what you pay for the fundamental prospects of a company, I have always felt that volatility is the price we pay for the trend we choose. In “GARP” investing (growth at a reasonable price), the goal is to buy as much future growth and quality returns on capital per unit of valuation as possible. Similarly, in trend following, we want to own the best performing trends per unit of volatility. In this case here, we can see that the overall trend score for this ETF, at 54, is not as of yet compensating the investor for the very poor volatility (average true range, or ATR) score.

On average then, it would seem that the ETF’s holdings have some heavy lifting to do if the ARKK is going to float back to the water’s surface. However, just as we were reminded this year that the S&P can be propelled higher by a handful of stocks while the rest of its constituents treaded water, is such an outcome possible for the ARKK ETF?

Anything is possible, but as the inset shows, the “cap-weighted” scores (Wgtd) are not much better. So, while entering a long position above $55, or even now before the breakout with a $45 stop, looks like an attractive setup on the surface, don’t lose sight of the fact that the ETF is just a portfolio of stocks. Barring a mini-MAG7 scenario, it would seem prudent to keep positions on the smaller side until the trend (TR) and momentum (MO) scores being to improve on average.

—

Originally posted on February 21st, 2024

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

Author(s)

David Lundgren, CMT, CFA

David Lundgren has more than three decades of investment industry experience, with a focus on technical analysis strategies, particularly momentum and trend following. He is the former Director of Technical Research…

Interest Rates and Their Potential Impact on Equities

Key Takeaways:

The repricing of rate cuts further out on the calendar has pushed 10-year Treasury yields higher. Technically, the next major area of overhead resistance sets up at the 4.35%–4.40% range.

Higher yields captured most of the blame for Tuesday’s equity market decline. However, it is not all bad news. Market expectations and Federal Reserve (Fed) monetary policy projections have become closer aligned, alleviating a source of market volatility. Furthermore, better-than-expected economic data has been a driving force of the market’s repricing of rate cuts, reducing the likelihood of a hard-landing scenario.

If yields continue higher, defensive sectors and international equity markets could notice a deterioration in relative strength, as they have been the most negatively correlated to 10-year yields over the last year. In contrast, these areas of the market could also witness an uptick in relative performance if yields pull back from their recent highs.

Investors have been playing a game of “how high will they go?”with Treasury yields this month. Better-than-expected economic data and Tuesday’s uptick in core consumer inflation have repriced Federal Fed rate-cut expectations further out on the calendar. Fed funds futures are now pricing in June as the most likely scenario for the first cut, as implied probabilities for a 25 basis-point rate cut in May are only around 50%. As a result, Treasury yields have shifted higher across the curve.

While higher yields captured most of the blame for Tuesday’s equity market sell-off, it is not all bad news. First, the gap between market expectations for rate cuts this year and Fed projections — a source of both equity and fixed income market volatility — has finally started to narrow. The market currently has priced in about four 25-basis-point (0.25%) cuts by year end, down from almost seven in January. The market is now only one cut away from the three cuts penciled in by the Fed during their December Summary of Economic Projections. Second, lowered expectations for rate cuts have been primarily underpinned by the economy doing better than expected. Of course, this raises inflation risk and the prospect for higher-for-longer monetary policy, both factors the market has successfully been dealing with over the last year.

Turning to the charts, 10-year yields have recaptured resistance from the January highs and 200-day moving average, leaving the 4.35%–4.40% range (prior highs/key retracement level) as the next major overhead resistance area. As highlighted below, yields have started to pull back from this area in the aftermath of Tuesday’s Consumer Price Index report. Support sets up at 4.20% and 4.12%.

While momentum indicators have turned bullish, trend strength remains questionable. As noted in the bottom panel of the chart below, the positive directional movement index (+DMI) crossed above the negative DMI (-DMI), pointing to a change in trend direction. However, the Average Directional Index (ADX) — used to measure trend strength (calculated from a smoothed average of the difference between the +DMI and -DMI) — remains low.

How High Will They Go?

Jump in 10-year Treasury Yields Hits Resistance

Source: LPL Research, Bloomberg 02/15/24

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Market Impact

With yields near a key area of overhead resistance, a breakout or breakdown from here could create many different outcomes for equity markets. To understand the impact of higher or lower rates on stocks, we analyzed the correlations between 10-year yields and several major market indexes and S&P 500 sectors. The table below breaks down each correlation.

As the table illustrates, higher rates would likely act as a headwind for the broader equity market landscape. Defensive sectors, such as utilities, consumer staples, and real estate may experience a deterioration in relative strength if yields break out, as they have been the most negatively correlated to yields over the last year. At the index level, global markets could also lag if yields continue higher. The MSCI All-Country World Index ex-USA is the most negatively correlated broad-market index to 10-year yields. In contrast, these areas of the market may experience an uptick in relative performance if yields pull back from their recent highs.

Source: LPL Research, Bloomberg 02/15/24

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Summary

Rising Treasury yields have recently run into a key area of overhead resistance. A breakout above the 4.35–4.40% range would not only be technically significant but also create headwinds for the broader equity market. If yields continue higher, defensive sectors and international equity markets could notice a deterioration in relative strength, and vice versa if yields pull back. Overall, starting yields for many fixed income markets are still at levels last seen over a decade ago, and LPL Research views the return prospects for fixed income as favorable and maintains its 3.75% to 4.25% year-end 2024 target for the 10-year Treasury yield.

Key Takeaways:

The repricing of rate cuts further out on the calendar has pushed 10-year Treasury yields higher. Technically, the next major area of overhead resistance sets up at the 4.35%–4.40% range.

Higher yields captured most of the blame for Tuesday’s equity market decline. However, it is not all bad news. Market expectations and Federal Reserve (Fed) monetary policy projections have become closer...

Author(s)

Adam Turnquist, CMT

As Vice President and Chief Technical Strategist, Adam Turnquist is responsible for the management and development of the technical research product within LPL Research. In this role, he provides LPL…

March: Historically Solid, but Plagued by Steep Losses in Election Years 1980 & 2020

As part of the Best Six/Eight Months featured in the 2024 Stock Trader’s Almanac, March has historically been a solid performing month with DJIA, S&P 500, NASDAQ, Russell 1000 & 2000 all advancing more than 64% of the time with average gains ranging from 0.7% by Russell 2000 to 1.1% by S&P 500.

March has a mixed track record in election years. Average performance is hammered lower by steep declines in 2020 and 1980. DJIA and S&P 500 have both advanced in 11 of the last 18 election-year Marchs, but the forementioned declines drag average performance to just 0.2% and 0.4% respectively. NASDAQ, Russell 1000 and Russell 2000 are hit even harder due to fewer years of data. Declines in 2020 were the result of the covid-19 pandemic while 1980’s losses can be attributed to surging inflation that peaked at 14.6%.

Subscribers to Almanac Investor get a full run down of seasonal tendencies that occur throughout each month of the year in an easy-to-read calendar graphic with important economic release dates highlighted, Daily Market Probability Index bullish and bearish days, market trends around options expiration and holidays. In addition, the Monthly Vital Statistics Table combines stats for the Dow, S&P 500, NASDAQ, Russell 1000 and Russell 2000 and puts them all in a single location available at the click of a mouse.

Author(s)

Jeffrey A. Hirsch

Jeffrey A. Hirsch is CEO of Hirsch Holdings and the editor-in-chief of the Stock Trader’s Almanac and Almanac Investor eNewsletter at www.stocktradersalmanac.com. Jeff is the author of The Little Book…

Cotton is forming a bull flag following last week’s breakout. Coffee futures are coiling below a critical polarity zone. Cattle and hogs are running wild. Even Dr.Copper is perking up, posting positive returns over the trailing five days.

And don’t forget about cocoa futures as they continue to print fresh all-time highs.

With all this action heating up, let’s turn our attention to one of 2021’s most explosive markets…

Lumber.

Remember all the lumber memes on Twitter?

Dudes were posting their W’s sitting atop stacks of 2x4s and plywood. I’ll never forget it.

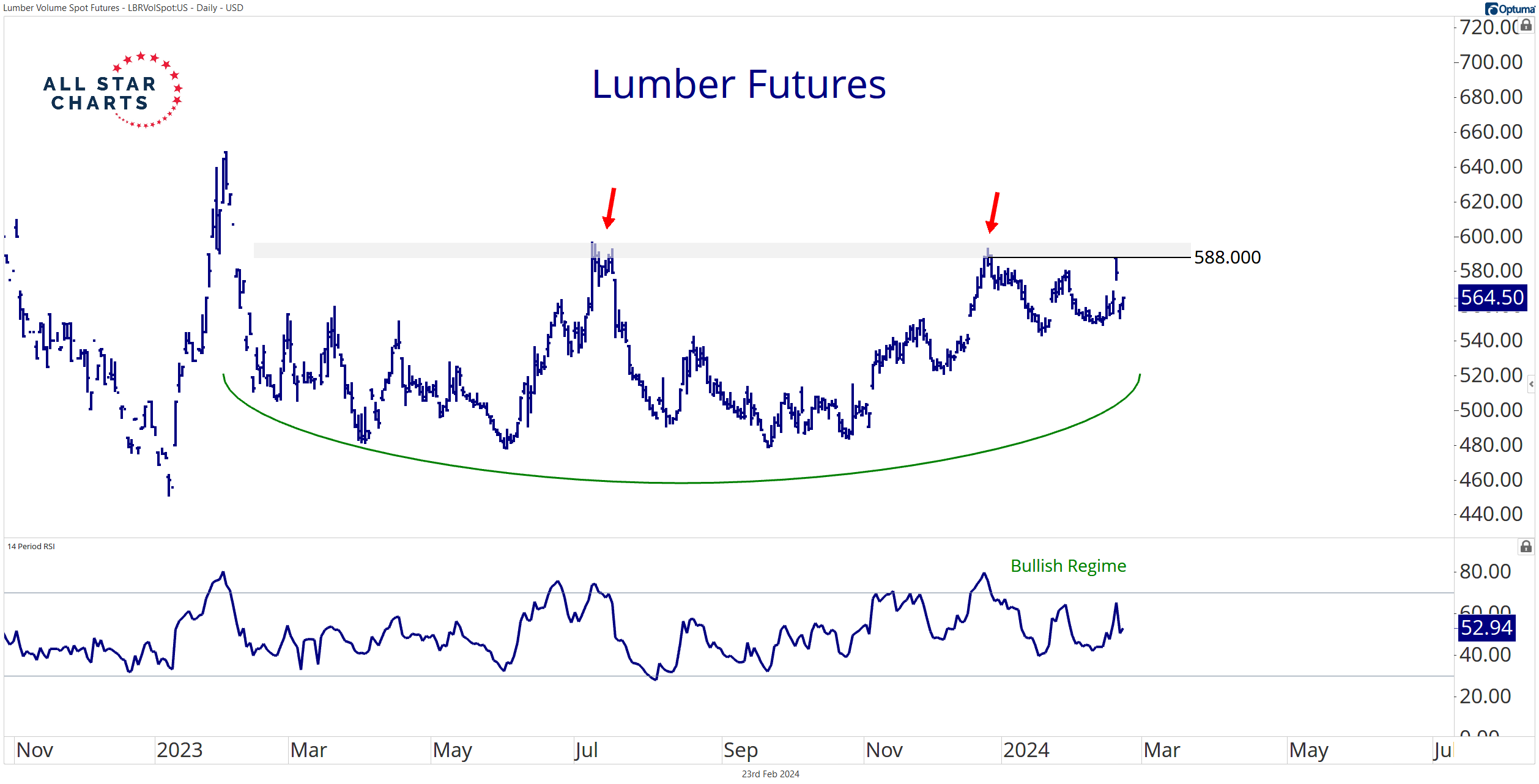

As a trader, I prefer to avoid lumber futures. It’s a thin market. But I can’t ignore the yearlong base forming on the daily chart:

Buyers are running into resistance at a shelf of former highs. A decisive close above 588.0 (Dec. closing high) flashes a buy signal.

Last year’s high stands as a logical initial target at approximately 650.0.

If lumber is in your wheelhouse, have a go. I won’t be taking this trade. It’s not for me.

Instead, I’m more interested in the information lumber futures provide.

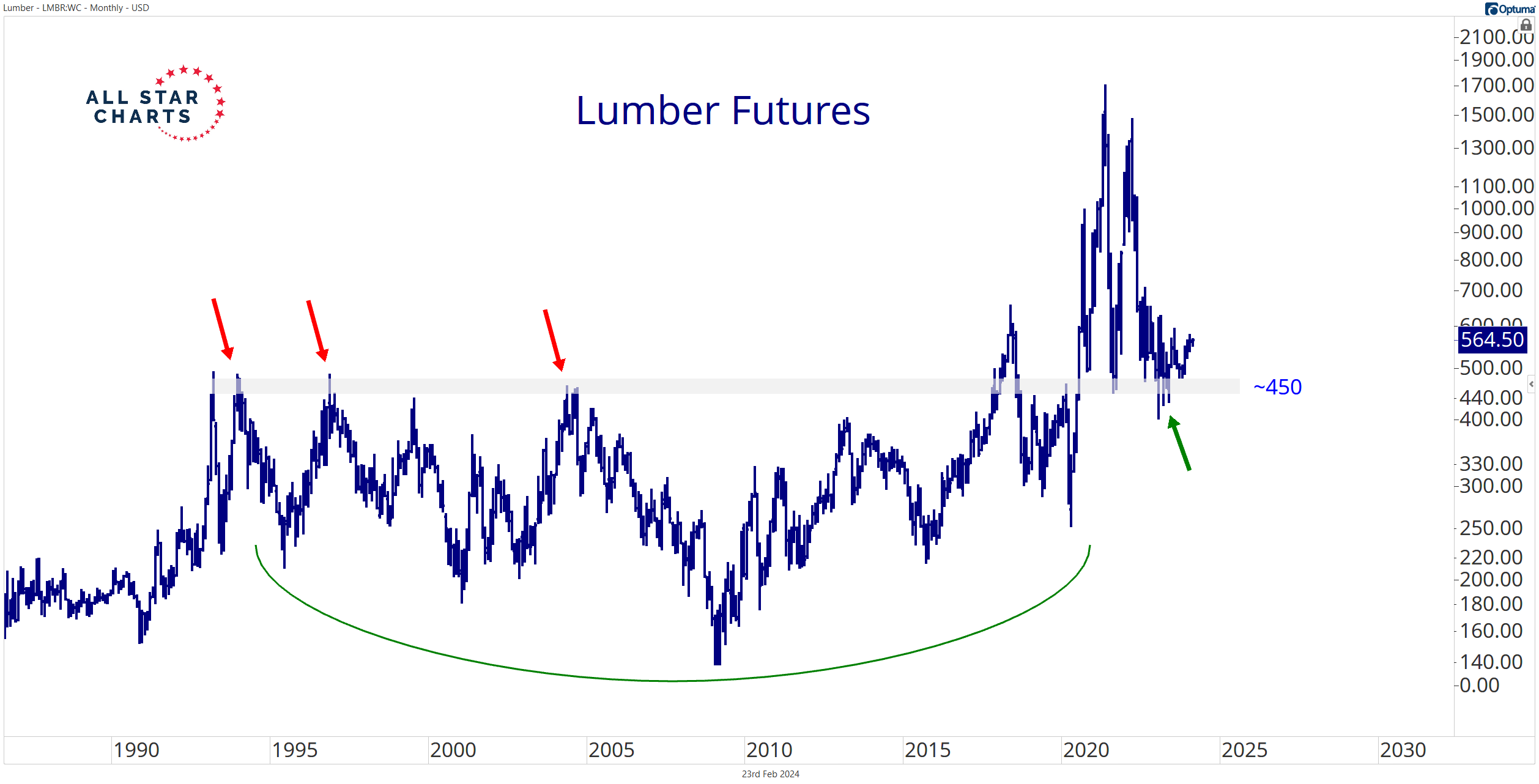

I view the 450 level as the lower bounds of a new generational range for lumber.

Other commodities will follow suit, breaking to new all-time highs while forming ranges that will define the coming decades.

It’s the type of price discovery that accompanies commodity supercycles.

On the other hand, lumber below 450 raises serious doubts regarding the current commodity bull run. It also wouldn’t support a healthy demand for economic-sensitive homebuilders.

There’s plenty to gain from tracking lumber’s next move, whether you choose to trade it or not.

But if you’re simply looking for a vehicle to express a bullish thesis for lumber, I have a setup for you in today’s commodity Trade of the Week…

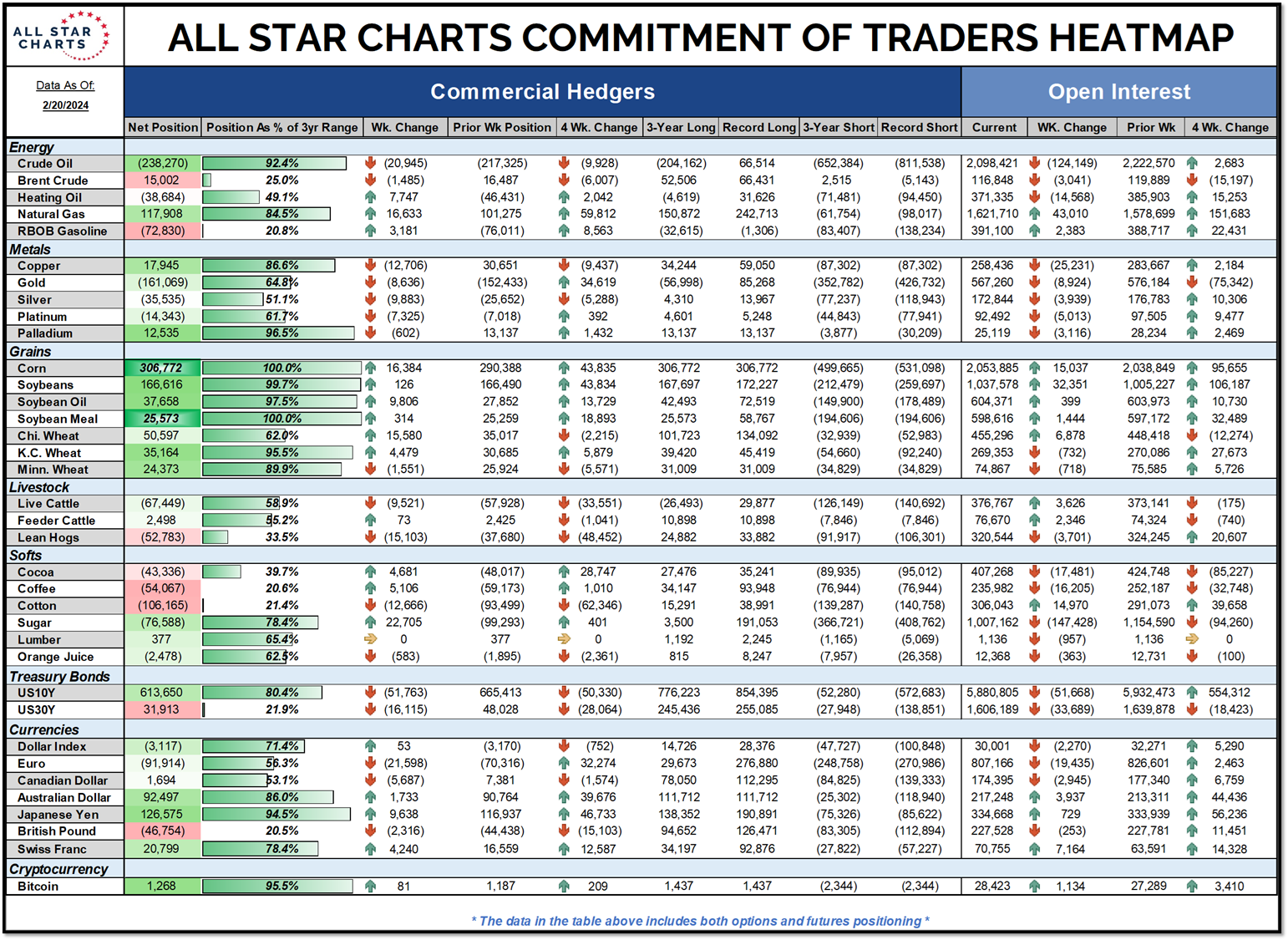

COT Heatmap Highlights

Commercial hedgers post another record-long position in corn.

Commercials’ long exposure to the Japanese yen falls within six percent of a new three-year extreme.

Commercial notch yet another record-long position for palladium, adding more than 2,000 contracts last week.

Cotton is forming a bull flag following last week’s breakout. Coffee futures are coiling below a critical polarity zone. Cattle and hogs are running wild. Even Dr.Copper is perking up, posting positive returns over the trailing five days.

And don’t forget about cocoa futures as they continue to print fresh all-time highs.

With all this action heating up, let’s turn our attention to one...

Author(s)

Ian Culley

Ian Culley is an investment analyst and Head of FICC at All Star Charts, focusing on Fixed income, Commodities, and Currencies. He began trading futures and forex in 2016, learning…

10-Year Treasury Rates: A Monthly/Secular Perspective Overview

I begin each year by reviewing the long-term technical positions and behaviors of what I think of as the “Big Four”—10-Year rates, S&P 500 ($SPX), Commodities, and the US Dollar. I believe that rates, particularly in a credit dependent/leveraged system, generally drive both the economic and market cycles. And, since by profession I am a rates/credit portfolio manager, strategist and trader, I always begin there.

Granted, a macro view doesn’t often inform short term trading, but anything that helps me understand the ebb and flow and interconnectedness of markets is helpful. More importantly, recognizing markets that are aligned for significant macro change can be invaluable, particularly in terms of risk management.

Since most good technical analysis is fractal, the same techniques used to describe the macro ebb and flow can often translate to shorter time frames. For the first two decades of my trading career I kept a manual grid of the big 4 plus a few other markets (gold, oil, 2-year Treasury and so forth) that I updated hourly with price and the change from the prior hour. By doing so, I learned a great deal about market interactions and interrelationships.

Monthly 10-Year Note Yield

<<A reminder that falling bond yields are synonymous with higher bond prices. In other words, a downtrend in yield = a bull market in bonds.>>

Over the last four decades bond yields had consistently and reliably made lower highs and lower lows. The entire bull market was defined by a broad declining channel (A–B, C–D). The A–B downtrend line represented the “stride of demand” or the zone where buyers consistently emerged and the C–D line represented the “overbought line” or the zone where supply or sellers consistently emerged.

From 2012 forward there were growing signs that the long downtrend was aging. Four things stood out.

The repeated failure to push to the oversold line (C–D).

The flattening out of the decline where each push to a new yield low only covered around 100 bps.

The 2018 spike to 3.24% that weakened the primary A-B downtrend.

In March of 2020 bonds pushed to the area around the center of the channel, failed to push beyond the midline much less into the overbought line (C–D). This change of behavior strongly suggested that demand was tiring. Multiple visible changes of behavior strongly suggested that the 40-year downtrend was in danger of terminating.

Now, the clear break and acceleration above the A–B downtrend has moved the long trend from bullish to neutral. While it’s likely that the move above November 2018 pivot @ 3.24% coupled with the prior changes of behavior mark the beginning of a long-term bear market, a higher low (perhaps forming in 2024) is needed to complete/confirm that change.

Note the additional changes in behavior. The 459 bps move from 0.39% to 4.98% represents the single largest bearish move since the inception of the bull market in September 1981, and the MACD oscillator level far exceeded the levels that marked yield highs over the course of the entire bull market.

10-Year Monthly with MACD

After producing the most overbought reading since the 1980s, the oscillator is trying to roll over and displaying a small negative divergence (suggesting lower yields and higher price). While not a definitive roll, it certainly suggests that there is some potential for a meaningful turn.

Monthly 10 Year Note Yield:

The following are several key fundamental points around rates:

The defining macro characteristic of the 40-year bull market has been the continual fall in the inflation rate. If that is changing (I believe that it has), the secular bond trend is likely to also change.

If the trend in inflation is changing, the negative correlation between bonds and equity that drives 60/40 allocation and risk parity investing is likely to flip and become positive. In other words, bonds and equity would, outside of periods of panic or economic distress, rise and fall together destroying the diversification benefit. This has been the historical norm and I expect that the market will gradually move in that direction.

The caveat being: Quantitative easing removed the value proposition from bonds, when equities began to decline in 2022 bonds couldn’t provide a safe haven. They were already far too expensive, particularly in the context of a Federal Reserve aggressively tightening monetary policy. That is no longer the case. Bonds, while still expensive, can again provide a tactical hedge should risk assets or the economy weaken dramatically.

At first glance, this seems at odds with the change in correlation discussed above, but it is a difference between the secular tide versus the intermediate wave.

Most substantive bond rallies are the result of a crisis that creates a flight-to-quality. In an economy that is overly financialized and levered, rising rates often break the weakest link in the economic chain, creating a new crisis and a subsequent flight to quality rally. While so far, there is little evidence of a systemic crisis, the lagged effect of the rapid increase in rates in an overly financialized system must be top of mind.

While there is still more work to be done to confirm the trend change, I believe the bond trend is finally changing as the world moves from the deflationary backdrop of the last several decades to an inflationary backdrop. I will be a much better seller of rallies and bearish technical setups in the weekly/intermediate perspective.

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

Author(s)

Stewart Taylor, CMT

Stewart Taylor is a Vice President, Portfolio Manager and a Senior Fixed Income Trader for the Investment Grade Fixed Income team at Eaton Vance Management in Boston, Massachusetts. He is…

CFA Institute Updates the Code of Ethics and Standards of Professional Conduct

The CMT Association adopted the CFA Institute’s Code of Ethics and Standards of Professional Conduct (Code and Standards) in 2015. This replaced the MTA Code of Ethics that had been in place until then. (You may read more about this change in the May 2015 issue of Technically Speaking.)

The CFA Institute recently updated the Code and Standards, effective January 1, 2024. The changes are not sweeping; rather, they are intended to clarify and address a few omissions. Here is a summary of the changes.

Within Standard I: Professionalism, the Board approved a new standard (I(E)) requiring members to act with and maintain the competence necessary to fulfill their professional responsibilities, so reinforcing the principle set forth in the Code of Ethics.

Within Standard V: Investment Analysis, Recommendations, and Actions, the Board revised Standard V(B) Communication with Clients and Prospective Clients, to require disclosures about the nature of the services provided by members and candidates and the costs to the client associated with those services (V(B 1)).

Within Standard VI Conflicts of Interest, the Board renamed Standard VI(A) “Avoid or Disclose Conflicts” and revised the standard to require members and candidates to either avoid conflicts of interest or disclose those conflicts. Previously there was no mention of avoiding conflicts of interest in the standard.

The CMT Association adopted the CFA Institute’s Code of Ethics and Standards of Professional Conduct (Code and Standards) in 2015. This replaced the MTA Code of Ethics that had been in place until then. (You may read more about this change in the May 2015 issue of Technically Speaking.)

The CFA Institute recently updated the Code and Standards, effective January 1, 2024. The...

Author(s)

Stanley Dash, CMT

Stanley Dash is the CMT Program Director at the CMT Association, a global credentialing body. In this role, Mr. Dash works with subject matter experts, candidates, and the Association’s members…

February has been an action-packed month for the CMT Association as we roll out two regional conferences across the world. The Board of Directors and the CMT staff both agreed at our Long-Range Planning meeting last August that we would focus our resources on delivering a series of regional conferences (globally) rather than a mega conference in New York City each year. The successful planning and execution of the 50th Annual Symposium in NYC last April was a monumental achievement, but we wanted to reach a wider audience in 2024 that may not have been able to make the trip to NYC.

The Mid-Winter Annual Retreat, held in Tampa on February 1st, provided over 100 attendees with a full day of presentations, interviews, trade idea discussion, and networking within our CMT community. The Association has had a full history dotted with mid-winter retreats ranging from Arizona to California to Florida; Tyler Wood and Bill Kelleher, who head up event planning, decided to rejuvenate that historical precedent by planning this event. I would like to personally thank Eric Caisse, who lives and works in Tampa and is a fellow Board member, for his effort in securing the event space and sponsorship dollars for the event. It is always enjoyable to see young technicians attend our events: we hosted a multitude of students from Florida Gulf Coast University under the stewardship of Ronald Mushock, CFA, their college professor, as they listened to Mark Dibble, Walter Deemer, Bob Farrell, and Craig Johnson among others present their lessons in technical analysis and risk management.

February has also kicked off the CMT’s Investment Challenge, which began on February 5th and will run until March 29th, with results being announced on April 5th. It is open to current CMT candidates and APP (Academic Partner Program) students. More than 525 candidates are registered for the Investment Challenge, and please keep track of results on the CMT’s LinkedIn page. If you need more information, please contact Kaizad Amrolia, Joel Pannikot, or Tyler Wood directly.

Lastly, the CMT Association is hosting an inaugural regional event in the Middle East region on February 28th and 29th. Dubai will be the location, and the Museum of the Future will be the venue. The Board of Directors and CMT Staff have been working on the logistics of this event for the last 6-8 months and I am sure it will not disappoint. There are nearly 200 registered attendees, speakers traveling from all over the globe, and the venue is second to none! After hosting such a fantastic event in NYC last April, I am beyond impressed that the CMT Association will be hosting its first event in what will hopefully become an extremely important strategic growth point for our Association. It is not too late to register if you are in the region!

I will be back in this space in March to discuss the results of the Dubai Symposium, several strategic growth focus points for the Association, and volunteer opportunities.

I had the privilege of speaking with the legendary Robert Farrell at the CMT Association’s Midwinter Retreat in Tampa. He recommended I read a book called One-Way Pockets: the book of books on Wall Street speculation. Published in 1917, it was written by Don Guyon, the fictitious name of a man working in a brokerage house during the War Bride bull market of 1915. It is my hope to relay some timeless market wisdom, study some market history, and share a book recommendation from our first president.

History & Background

The year is 1915. Electricity, the internal combustion engine, running water in our homes, and the desire for city life over rural life are all changing the way we live. US equities have been in a secular trading range since 1900. We are in the midst of the War Bride bull market following the start of World War 1. See chart 1.

Chart 1

World War 1 officially started on July 28th, 1914. Trading on the New York Stock Exchange closed from July 30th to December 12th, 1914, as foreign investors began liquidating their holdings to raise money to fund the war. When trading resumed, The Dow Industrial average gained more than 86% over 257 trading days. This rally was fueled by the government as it began spending heavily to produce goods for the Europeans to purchase to support the war. The 1915 rally was led by the aptly named War Bride stocks, including munition, iron, steel, shipping, and textiles. See chart 2.

Don Guyon (DG), working in a brokerage house in December 1915, had a difficult time understanding why speculators were losing money at the end of such a spectacular bull run. To figure this out, he went through the accounts of six of the brokerage’s largest active traders. He analyzed their transactions from July 1st, 1915, to February 29th, 1916. See chart 2. He concluded, “…the trading methods of each [speculator] had undergone a pronounced and obviously unintentional change with the progress of the bull market from one stage to another”1

Chart 2

After doing his study by analyzing his brokerage’s order book, DG concluded that the speculators’ behavior was backwards. They were doing the exact opposite of what they should have.

When the bull market was in its infancy, DG found that speculators were taking quick, small profits and small losses. They were also using stop orders for protection.

As the bull market continued, they repurchased these stocks at higher prices. This time though, they took profits on larger gains than before. Some lost money by shorting in an attempt to call the top.

Even further into the bull market, speculators stopped taking any profits at all. They also stopped using protective stop orders, even as stocks doubled. The speculators did not want to be stopped out again.

They sold too soon, repurchased at higher prices, quit using stops, bought more stock after the market finally started distribution, and sold long positions on breaks lower instead of on rallies.

Before we get to DG’s trading methodology, he eventually offers the following regarding a speculator’s psychology. “The operating method I have outlined is not fool-proof or otherwise infallible… But the speculator who adhered closely to its rules may at least rest assured that his trading methods are diametrically opposed to the trading methods of the great majority of speculators – and the great majority of speculators are, as we know, consistent losers in Wall Street.”2

and

“The man who applies this or any other speculative method successfully must be able to exercise patience and self-control, to withstand all forms of mental temptation, to ignore the dictates of fear and greed, and to disregard everything he hears, sees, or reads that may cause the slightest deviation from his course.”3

and

“The few who make money in the stock market await what they consider exceptional opportunities and then play for profits that are worthwhile. They look ahead a week or a month or a year, as the case may be, and disregard the changes that occur in the price movement in each daily session, which to the daily trader assumes exaggerated proportions.”4

DG’s Plan to Speculate Covering a Complete Market Cycle

First determine the trend of the overall market, and then speculate in that direction. Be careful of rangebound markets, but if desired buy low and sell high.

How a bull market starts/when to get long:

Most speculators become convinced of a bull swing when it approaches its culmination.

Bull markets start after a protracted period of dullness and narrow fluctuations. Price breaks through the trading range with increased activity on the advances. Sometimes many stocks advance, while at other times the advance is narrow. Look for leaders entering new high territory as confirmation.

Bull markets might also begin after a period of declining prices when the market advances or refuses to go down on bad news. Look for when the market finally advances above the point where it was before the bad news as confirmation.

DG also tells us:

It is just as important to determine what to buy as when to buy. He recommends two or three active stocks, and he recommends buying stocks that have declined the least.

Write a trading plan before making any commitments. He reminds us that our judgement is most logical before having money in the market, which tends to warp ones sound judgement.

Use protective stop orders, and enter them at the same time as buy orders. Never lower or cancel them. Raise them in accordance with your predetermined plan. Set them based on market action/price. They should take you out of your positions when your idea is no longer valid, not based on an arbitrary number of points or a percentage.

Follow the plan. Do not change the plan because of news, market action, or any other outside influence based on things we hear, read, feel, etc…

Seeing the first reaction through:

You are now long. Your stocks have advanced for several days. DG tells us:

Do not make the mistake of trying to find the top and play for a reaction.

Do not sell, even if you are convinced the advance has gone too far too fast. This is the opposite advice of the cliche’, nobody ever goes broke taking a profit. He disagrees.

Stay invested as the issue pulls back 50% or more.

Add on strength when the price begins to resume its advance and the correction appears over. This second purchase should also have a protective stop.

The first selling point:

Your original line of long stock should be sold on the recovery to the former highs, while the stock bought on the reaction should be retained.

This process of buying shares on strength after pullbacks and selling shares at the previous swing highs should be repeated as long as the market continues to advance into new high territory.

Do not make purchases at new highs. “…this temptation is fatal alike to his mental attitude and the success of his operations.”5

The great distributive stage:

The market usually has several successive days in which the volume of sales is very large and speculative excitement is intense.

Stocks under distribution will have sharp but short-lived advances, followed by gradual declines.

There will come a time when, instead of resuming the advance, stocks will go sideways near their previous top. The action will look similar to the past and the public will again buy. This is the time to exit your position. Stock has been transferred from the strong hands to the weak hands.

Exit your position.

If this is happening at the broad market level, it is time to “get out of all stocks and stay out, regardless of the strength displayed by certain issues… Not only is this the time to sell long stock, it is also the time to put out a line of shorts.”6

When and what to sell short:

In contrast to buying stocks long, look to short the weakest issues. These are the ones breaking down from ranges well below their highs instead of at or near their highs.

Limit your losses using stops, just as you did on the long side.

Use the same tactics as longs, just in the opposite direction.

Remember, when selling short, rallies will be very, very sharp. Instead of covering too early, “cover your complete line only when the market no longer goes down on bad news or when it moves upward through a trading area…”7

Final Thoughts

DG’s perspective is a fascinating one. He studied actual buy and sell orders of unsuccessful speculators, and then he crafted trading guidelines which do the exact opposite of what they did. He shared important psychological ideas. He even made the case for Technical Analysis as a discipline: “To tell a speculator to base his operations on his interpretation of fundamental factors is to leave him just where he started…The market itself determines the relative importance of all factors more accurately.”8

I encourage you to read this book, and I again thank Mr. Farrell for this recommendation. In closing, DG tells us, and I believe Mr. Farrell would agree, “…the only speculative method that would prove profitable in the long run must be the reverse of that followed by the consistently unsuccessful public.”9

References

Guyon, Don. One-Way Pockets: the book of books on Wall Street speculation. New York, New York: Cosimo, 2005. Page 16.

In yesterday’s missive, using the simple formula P=(F*V)S, I highlighted the inviolable link between long-term trends in both stock prices and fundamentals, and how all good things that happen to price begin with superior fundamentals, valuation expansion, and optimistic sentiment. “Multi-baggers” happen when price benefits from simultaneous improvements in all three of these inputs. However, I also drew a fine line yesterday between fundamentals and opinions of fundamentals, and how, in my view, the only opinion that matters is that of the market, or price trend itself.

Why is that? Because no matter what one thinks about a company’s future growth prospects and present valuation, that opinion will never be monetized favorably until the market agrees with it, via a strong price trend and relative outperformance.

In accordance with this philosophy then, investors should populate their portfolios with stocks that meet as many of these “multi-bagger” criteria as possible. The Venn diagram of long-term winners featured below provides a simple framework for thinking about this objective. Ideally, a portfolio will be full of “1s”, a smattering of “2s”, and perhaps a few “3s”. Most importantly however, “4s” should be avoided at all costs.

Some investors gain the greatest comfort from being contrarian, buying stocks when they are outside of the “Price Trend & Momentum” circle (i.e., “4s”). Of course, this might work out from time to time, but one of the few guarantees in this business is that no stock will everbe a multi-bagger without first making its way back into this circle. Let’s therefore call it the “Winner’s Circle”.

One can lean on this concept to assess the future prospects of an ETF, for instance. By mapping the holdings of an ETF to this Venn diagram of long-term winners, we can qualify whether or not the portfolio is positioned for future success.

By way of example, the ARK Innovation ETF (ARKK) chart pattern (below) would likely be identified by most technicians as a complex head & shoulders bottom, and I would agree. Another rotation higher, with a close above $55 would open the door to a run to the pattern’s upside target in the $95-$100 area (green box), which also overlaps with the Q1’21 lows, as well as the zone between a 50% and 62% retracement of the roughly -80% decline from 2022-2023.

Like the S&P itself, this ETF can only achieve that objective if the stocks within it are up for the challenge. In the” P=F*V” framework (inset in chart above), we can see that the average (Avg) trend score (TR) and momentum score (MO) hover just above average at 54 and 58, respectively.

In terms of fundamentals (F), using data from Koyfin.com, we can simply calculate the growth quality (GQ) and returns quality (RQ) of each stock compared to the rest of the market. Befitting the manager’s style, we can see that the average stock’s GQ score is far greater than its current RQ score (73 & 34, respectively). This suggests that the manager’s expectation is that these stocks, on average, will grow themselves into profitability, a characteristic mindset of those investors trafficking in the disruptive technology space.

Finally, we have valuation (V). Here, we can see that the average stock in the portfolio scores rather poorly from a valuation (VA) perspective relative to the rest of the market (14). This too is almost par for the course for hyper growth investors, banking that stocks that look expensive today are likely to look cheap in hindsight once the expected growth and profitability come through. In history, Amazon was a good example of this, where famed value investor Bill Miller was ridiculed and chastised for owning Amazon in the Legg Mason Value Fund. He pushed back saying it was inexpensive based on future growth, and boy was he ever proven right!

Just as the price-earnings ratio (PE) is what you pay for the fundamental prospects of a company, I have always felt that volatility is the price we pay for the trend we choose. In “GARP” investing (growth at a reasonable price), the goal is to buy as much future growth and quality returns on capital per unit of valuation as possible. Similarly, in trend following, we want to own the best performing trends per unit of volatility. In this case here, we can see that the overall trend score for this ETF, at 54, is not as of yet compensating the investor for the very poor volatility (average true range, or ATR) score.

On average then, it would seem that the ETF’s holdings have some heavy lifting to do if the ARKK is going to float back to the water’s surface. However, just as we were reminded this year that the S&P can be propelled higher by a handful of stocks while the rest of its constituents treaded water, is such an outcome possible for the ARKK ETF?

Anything is possible, but as the inset shows, the “cap-weighted” scores (Wgtd) are not much better. So, while entering a long position above $55, or even now before the breakout with a $45 stop, looks like an attractive setup on the surface, don’t lose sight of the fact that the ETF is just a portfolio of stocks. Barring a mini-MAG7 scenario, it would seem prudent to keep positions on the smaller side until the trend (TR) and momentum (MO) scores being to improve on average.

—

Originally posted on February 21st, 2024

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

Interest Rates and Their Potential Impact on Equities

Key Takeaways:

The repricing of rate cuts further out on the calendar has pushed 10-year Treasury yields higher. Technically, the next major area of overhead resistance sets up at the 4.35%–4.40% range.

Higher yields captured most of the blame for Tuesday’s equity market decline. However, it is not all bad news. Market expectations and Federal Reserve (Fed) monetary policy projections have become closer aligned, alleviating a source of market volatility. Furthermore, better-than-expected economic data has been a driving force of the market’s repricing of rate cuts, reducing the likelihood of a hard-landing scenario.

If yields continue higher, defensive sectors and international equity markets could notice a deterioration in relative strength, as they have been the most negatively correlated to 10-year yields over the last year. In contrast, these areas of the market could also witness an uptick in relative performance if yields pull back from their recent highs.

Investors have been playing a game of “how high will they go?”with Treasury yields this month. Better-than-expected economic data and Tuesday’s uptick in core consumer inflation have repriced Federal Fed rate-cut expectations further out on the calendar. Fed funds futures are now pricing in June as the most likely scenario for the first cut, as implied probabilities for a 25 basis-point rate cut in May are only around 50%. As a result, Treasury yields have shifted higher across the curve.

While higher yields captured most of the blame for Tuesday’s equity market sell-off, it is not all bad news. First, the gap between market expectations for rate cuts this year and Fed projections — a source of both equity and fixed income market volatility — has finally started to narrow. The market currently has priced in about four 25-basis-point (0.25%) cuts by year end, down from almost seven in January. The market is now only one cut away from the three cuts penciled in by the Fed during their December Summary of Economic Projections. Second, lowered expectations for rate cuts have been primarily underpinned by the economy doing better than expected. Of course, this raises inflation risk and the prospect for higher-for-longer monetary policy, both factors the market has successfully been dealing with over the last year.

Turning to the charts, 10-year yields have recaptured resistance from the January highs and 200-day moving average, leaving the 4.35%–4.40% range (prior highs/key retracement level) as the next major overhead resistance area. As highlighted below, yields have started to pull back from this area in the aftermath of Tuesday’s Consumer Price Index report. Support sets up at 4.20% and 4.12%.

While momentum indicators have turned bullish, trend strength remains questionable. As noted in the bottom panel of the chart below, the positive directional movement index (+DMI) crossed above the negative DMI (-DMI), pointing to a change in trend direction. However, the Average Directional Index (ADX) — used to measure trend strength (calculated from a smoothed average of the difference between the +DMI and -DMI) — remains low.

How High Will They Go?

Jump in 10-year Treasury Yields Hits Resistance

Source: LPL Research, Bloomberg 02/15/24

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Market Impact

With yields near a key area of overhead resistance, a breakout or breakdown from here could create many different outcomes for equity markets. To understand the impact of higher or lower rates on stocks, we analyzed the correlations between 10-year yields and several major market indexes and S&P 500 sectors. The table below breaks down each correlation.

As the table illustrates, higher rates would likely act as a headwind for the broader equity market landscape. Defensive sectors, such as utilities, consumer staples, and real estate may experience a deterioration in relative strength if yields break out, as they have been the most negatively correlated to yields over the last year. At the index level, global markets could also lag if yields continue higher. The MSCI All-Country World Index ex-USA is the most negatively correlated broad-market index to 10-year yields. In contrast, these areas of the market may experience an uptick in relative performance if yields pull back from their recent highs.

Source: LPL Research, Bloomberg 02/15/24

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Summary

Rising Treasury yields have recently run into a key area of overhead resistance. A breakout above the 4.35–4.40% range would not only be technically significant but also create headwinds for the broader equity market. If yields continue higher, defensive sectors and international equity markets could notice a deterioration in relative strength, and vice versa if yields pull back. Overall, starting yields for many fixed income markets are still at levels last seen over a decade ago, and LPL Research views the return prospects for fixed income as favorable and maintains its 3.75% to 4.25% year-end 2024 target for the 10-year Treasury yield.

March: Historically Solid, but Plagued by Steep Losses in Election Years 1980 & 2020

As part of the Best Six/Eight Months featured in the 2024 Stock Trader’s Almanac, March has historically been a solid performing month with DJIA, S&P 500, NASDAQ, Russell 1000 & 2000 all advancing more than 64% of the time with average gains ranging from 0.7% by Russell 2000 to 1.1% by S&P 500.

March has a mixed track record in election years. Average performance is hammered lower by steep declines in 2020 and 1980. DJIA and S&P 500 have both advanced in 11 of the last 18 election-year Marchs, but the forementioned declines drag average performance to just 0.2% and 0.4% respectively. NASDAQ, Russell 1000 and Russell 2000 are hit even harder due to fewer years of data. Declines in 2020 were the result of the covid-19 pandemic while 1980’s losses can be attributed to surging inflation that peaked at 14.6%.

Subscribers to Almanac Investor get a full run down of seasonal tendencies that occur throughout each month of the year in an easy-to-read calendar graphic with important economic release dates highlighted, Daily Market Probability Index bullish and bearish days, market trends around options expiration and holidays. In addition, the Monthly Vital Statistics Table combines stats for the Dow, S&P 500, NASDAQ, Russell 1000 and Russell 2000 and puts them all in a single location available at the click of a mouse.

Cotton is forming a bull flag following last week’s breakout. Coffee futures are coiling below a critical polarity zone. Cattle and hogs are running wild. Even Dr.Copper is perking up, posting positive returns over the trailing five days.

And don’t forget about cocoa futures as they continue to print fresh all-time highs.

With all this action heating up, let’s turn our attention to one of 2021’s most explosive markets…

Lumber.

Remember all the lumber memes on Twitter?

Dudes were posting their W’s sitting atop stacks of 2x4s and plywood. I’ll never forget it.

As a trader, I prefer to avoid lumber futures. It’s a thin market. But I can’t ignore the yearlong base forming on the daily chart:

Buyers are running into resistance at a shelf of former highs. A decisive close above 588.0 (Dec. closing high) flashes a buy signal.

Last year’s high stands as a logical initial target at approximately 650.0.

If lumber is in your wheelhouse, have a go. I won’t be taking this trade. It’s not for me.

Instead, I’m more interested in the information lumber futures provide.

I view the 450 level as the lower bounds of a new generational range for lumber.

Other commodities will follow suit, breaking to new all-time highs while forming ranges that will define the coming decades.

It’s the type of price discovery that accompanies commodity supercycles.

On the other hand, lumber below 450 raises serious doubts regarding the current commodity bull run. It also wouldn’t support a healthy demand for economic-sensitive homebuilders.

There’s plenty to gain from tracking lumber’s next move, whether you choose to trade it or not.

But if you’re simply looking for a vehicle to express a bullish thesis for lumber, I have a setup for you in today’s commodity Trade of the Week…

COT Heatmap Highlights

Commercial hedgers post another record-long position in corn.

Commercials’ long exposure to the Japanese yen falls within six percent of a new three-year extreme.

Commercial notch yet another record-long position for palladium, adding more than 2,000 contracts last week.

10-Year Treasury Rates: A Monthly/Secular Perspective Overview

I begin each year by reviewing the long-term technical positions and behaviors of what I think of as the “Big Four”—10-Year rates, S&P 500 ($SPX), Commodities, and the US Dollar. I believe that rates, particularly in a credit dependent/leveraged system, generally drive both the economic and market cycles. And, since by profession I am a rates/credit portfolio manager, strategist and trader, I always begin there.

Granted, a macro view doesn’t often inform short term trading, but anything that helps me understand the ebb and flow and interconnectedness of markets is helpful. More importantly, recognizing markets that are aligned for significant macro change can be invaluable, particularly in terms of risk management.

Since most good technical analysis is fractal, the same techniques used to describe the macro ebb and flow can often translate to shorter time frames. For the first two decades of my trading career I kept a manual grid of the big 4 plus a few other markets (gold, oil, 2-year Treasury and so forth) that I updated hourly with price and the change from the prior hour. By doing so, I learned a great deal about market interactions and interrelationships.

Monthly 10-Year Note Yield

<<A reminder that falling bond yields are synonymous with higher bond prices. In other words, a downtrend in yield = a bull market in bonds.>>

Over the last four decades bond yields had consistently and reliably made lower highs and lower lows. The entire bull market was defined by a broad declining channel (A–B, C–D). The A–B downtrend line represented the “stride of demand” or the zone where buyers consistently emerged and the C–D line represented the “overbought line” or the zone where supply or sellers consistently emerged.

From 2012 forward there were growing signs that the long downtrend was aging. Four things stood out.

The repeated failure to push to the oversold line (C–D).

The flattening out of the decline where each push to a new yield low only covered around 100 bps.

The 2018 spike to 3.24% that weakened the primary A-B downtrend.

In March of 2020 bonds pushed to the area around the center of the channel, failed to push beyond the midline much less into the overbought line (C–D). This change of behavior strongly suggested that demand was tiring. Multiple visible changes of behavior strongly suggested that the 40-year downtrend was in danger of terminating.

Now, the clear break and acceleration above the A–B downtrend has moved the long trend from bullish to neutral. While it’s likely that the move above November 2018 pivot @ 3.24% coupled with the prior changes of behavior mark the beginning of a long-term bear market, a higher low (perhaps forming in 2024) is needed to complete/confirm that change.

Note the additional changes in behavior. The 459 bps move from 0.39% to 4.98% represents the single largest bearish move since the inception of the bull market in September 1981, and the MACD oscillator level far exceeded the levels that marked yield highs over the course of the entire bull market.

10-Year Monthly with MACD

After producing the most overbought reading since the 1980s, the oscillator is trying to roll over and displaying a small negative divergence (suggesting lower yields and higher price). While not a definitive roll, it certainly suggests that there is some potential for a meaningful turn.

Monthly 10 Year Note Yield:

The following are several key fundamental points around rates:

The defining macro characteristic of the 40-year bull market has been the continual fall in the inflation rate. If that is changing (I believe that it has), the secular bond trend is likely to also change.

If the trend in inflation is changing, the negative correlation between bonds and equity that drives 60/40 allocation and risk parity investing is likely to flip and become positive. In other words, bonds and equity would, outside of periods of panic or economic distress, rise and fall together destroying the diversification benefit. This has been the historical norm and I expect that the market will gradually move in that direction.

The caveat being: Quantitative easing removed the value proposition from bonds, when equities began to decline in 2022 bonds couldn’t provide a safe haven. They were already far too expensive, particularly in the context of a Federal Reserve aggressively tightening monetary policy. That is no longer the case. Bonds, while still expensive, can again provide a tactical hedge should risk assets or the economy weaken dramatically.

At first glance, this seems at odds with the change in correlation discussed above, but it is a difference between the secular tide versus the intermediate wave.

Most substantive bond rallies are the result of a crisis that creates a flight-to-quality. In an economy that is overly financialized and levered, rising rates often break the weakest link in the economic chain, creating a new crisis and a subsequent flight to quality rally. While so far, there is little evidence of a systemic crisis, the lagged effect of the rapid increase in rates in an overly financialized system must be top of mind.

While there is still more work to be done to confirm the trend change, I believe the bond trend is finally changing as the world moves from the deflationary backdrop of the last several decades to an inflationary backdrop. I will be a much better seller of rallies and bearish technical setups in the weekly/intermediate perspective.

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

CFA Institute Updates the Code of Ethics and Standards of Professional Conduct

The CMT Association adopted the CFA Institute’s Code of Ethics and Standards of Professional Conduct (Code and Standards) in 2015. This replaced the MTA Code of Ethics that had been in place until then. (You may read more about this change in the May 2015 issue of Technically Speaking.)

The CFA Institute recently updated the Code and Standards, effective January 1, 2024. The changes are not sweeping; rather, they are intended to clarify and address a few omissions. Here is a summary of the changes.

Within Standard I: Professionalism, the Board approved a new standard (I(E)) requiring members to act with and maintain the competence necessary to fulfill their professional responsibilities, so reinforcing the principle set forth in the Code of Ethics.

Within Standard V: Investment Analysis, Recommendations, and Actions, the Board revised Standard V(B) Communication with Clients and Prospective Clients, to require disclosures about the nature of the services provided by members and candidates and the costs to the client associated with those services (V(B 1)).

Within Standard VI Conflicts of Interest, the Board renamed Standard VI(A) “Avoid or Disclose Conflicts” and revised the standard to require members and candidates to either avoid conflicts of interest or disclose those conflicts. Previously there was no mention of avoiding conflicts of interest in the standard.

{kind=link}