JOURNAL OF

TECHNICAL ANALYSIS

Issue 67, 2013

Editorial Board

Stanley Dash, CMT

CMT Program Director

Fred Meissner, CMT

Founder & President, The Fred Report

David Aronson, CMT

President, Hood River Research

Kevin J. Lapham, CMT

Portfolio Manager

Kristin Hetzer, CMT, CIMA, CFP

Principal and Owner, Royal Palms Capital LLC

Richard J. Bauer, Jr. Ph.D., CMT, CFA

Professor, Finance, St. Mary’s University

Jeremy du Plessis, CMT, FSTA

Head of Technical Analysis and Product Development, Updata Ltd.

Cynthia A Kase, CMT, MFTA

Expert Consultant

Saeid Mokhtari, CMT

Market Research Analyst, CIBC World Markets

Gordon Scott, CMT

Carson Dahlberg, CMT

Partner, Northington Dahlberg Research

CMT Association, Inc.

25 Broadway, Suite 10-036, New York, New York 10004

www.cmtassociation.org

Published by Chartered Market Technician Association, LLC

ISSN (Print)

ISSN (Online)

The Journal of Technical Analysis is published by the Chartered Market Technicians Association, LLC, 25 Broadway, Suite 10-036, New York, NY 10004.New York, NY 10006. Its purpose is to promote the investigation and analysis of the price and volume activities of the world’s financial markets. The Journal of Technical Analysis is distributed to individuals (both academic and practicitioner) and libraries in the United States, Canada, and several other countries in Europe and Asia. Journal of Technical Analysis is copyrighted by the CMT Association and registered with the Library of Congress. All rights are reserved.

Table of Contents

JOTA ISSUE 67, 2013

Letter from the Editor

by Julie Dahlquist, Ph.D., CMT

Letter from the Editor

by Julie Dahlquist, Ph.D., CMT

Greetings from the Editor!

The mission of the Journal of Technical Analysis (JOTA) is to advance the knowledge and understanding of the practice of technical analysis through the publication of well-crafted, high-quality papers in all areas of technical analysis. While the MTA membership is the primary audience for the journal, the readership reaches far beyond the organization. The journal’s presence in libraries and electronic databases allows both practitioners and academics around the world to access its content.

The articles in this issue highlight the diversity of topics which are of interest to the technical analyst. George Schade provides a history of the development of the advance-decline indicators. The MTA is a leader in providing a record of these historical developments for future generations of technical analysts. George’s article also reminds us that observing the market and asking simple questions can lead to timeless indicators. Gregory Kuhlemeyer and Robert Kunkel demonstrate how the classic notion of momentum can be used as a trading tool in a specific market. The article by Camillo Lento highlights how the application of other fields, such as fractal geometry, can increase our understanding of the market.

In addition to these three new articles, we are printing the 2010 and 2011 Charles H. Dow Award winning papers in this issue. Wayne Whaley’s paper, “Planes, Trains, and Automobiles: A Study of Various Market Thrust Measures,” analyzes the use of thrust and capitulation measures as tools for gauging the potential for sizable intermediate market moves. “Analyzing Gaps for Profitable Trading Strategies,” written by Richard Bauer and me, provides insight into the price movement that tends to occur after a stock gaps up or down.

The production of an issue is a complex process, requiring the assistance of many individuals. Of course, a journal begins with authors who desire to share their knowledge, expertise, and experience with the broader community of technical analysts. But, that is just the beginning. Once papers are submitted for consideration, they are subjected to a double-blind review process. In this process, papers are reviewed by at least two experts who provide feedback regarding the accuracy of the work as well as gauge the suitability of the piece for publication in the Journal of Technical Analysis. This is known as a double-blind review process because the reviewers do not know the identity of the author and the author does not know the identity of the reviewers. In addition, the staff at the MTA office provides significant support in the production and distribution process. I would like to thank all of those who contributed to this process. If you are considering submitting an article for a future issue, or if you would like to serve as a reviewer, let me know.

Julie Dahlquist, Ph.D., CMT

Analyzing Gaps for Profitable Trading Strategies

by Julie Dahlquist, Ph.D., CMT

About the Author | Julie Dahlquist, Ph.D., CMT

Julie Dahlquist, Ph.D., CMT is Professor of Professional Practice in the Finance Department at Texas Christian University (TCU). Previously, she served on the faculty in the business schools at University of Texas at San Antonio and at St. Mary’s University. Her teaching experience spans over three decades and includes undergraduate, graduate, and Executive MBA students in programs in Mexico, Austria, Germany, Switzerland, Italy, Belgium, Greece and South Korea.

Julie is the president of the Technical Analysis Educational Foundation which works with colleges and universities to include technical analysis as an integral part of their finance curriculum. Her research has appeared in Financial Analysts Journal, Managerial Finance, Applied Economics, Working Money, Financial Practices and Education, and the Journal of Financial Education. She has served as editor of the Journal of Technical Analysis and on the editorial board of the Southwestern Business Administration Journal, as well as a reviewer for a number of other journals.

Julie has co-authored Technical Analysis: The Complete Resource for Financial Market Technicians with Charles Kirkpatrick and two books: Technical Analysis of Gaps and Technical Market Indicators: Analysis and Performance with Richard Bauer. She is the recipient of the Charles H. Dow Award for research in technical analysis and the Mike Epstein Award for promoting technical analysis in academia.

Julie graduated from the University of Louisiana at Monroe with a B.B.A. with major in economics, summa cum laude. She received her M.A. in theology from St. Mary’s University and her Ph.D. in economics from Texas A&M University.

by Richard J. Bauer, Jr. Ph.D., CMT, CFA

About the Author | Richard J. Bauer, Jr. Ph.D., CMT, CFA

Richard J. Bauer, Jr. Ph.D., CFA, CMT is Professor of Finance at the Bill Greehey School of Business at St. Mary’s University in San Antonio, Texas. He is the author of three books: Genetic Algorithms and Investment Strategies, Technical Market Indicators (with Julie Dahlquist), and Technical Analysis of Gaps (with Julie Dahlquist). He and Julie won the CMT Association’s Charles Dow Award in 2011.

Gaps have attracted the attention of market technicians since the earliest days of stock charting. A gap up occurs when today’s low is greater than yesterday’s high (See Gap A in Figure 1). A gap down occurs when today’s high is lower than yesterday’s low (See Gap B in Figure 1.). A gap creates a hole in a daily price bar chart. This gap is called a “window” when using candlestick charts. A gap up is referred to as a “rising window” and is considered a bullish signal. A “falling window,” which is a gap down, gives a bearish signal. (Nison, 2001)

It is easy to understand why early technicians noticed gaps; gaps are conspicuous on a stock chart. However, technicians did not just pay attention because they were easy to spot. Because gaps show that price has jumped, they may represent some significant change in what is happening with the stock and signal a trading opportunity. According to Edwards and Magee, the importance attached to gaps was unfortunate because

there soon accumulated a welter of ‘rules’ for their interpretation some of which have acquired an almost religious force and are cited by the superficial chart reader with little understanding as to why they work when they work (and, of course, as is always the case with any superstition, an utter disregard of those instances where they don’t work).

Edwards and Magee, 1966, p 190

Given the persistence of some of these superstitions, such as “a gap must be closed,” surprisingly little study has been undertaken to analyze the effectiveness of using gaps in trading. In this paper we provide a comprehensive study of gaps in an attempt to isolate gaps which present profitable trading strategies.

Literature Review

Breakaway gaps occur when price suddenly breaks through a formation boundary and signal the beginning of a trend. These are thought to be the most profitable gaps. In fact, David Landry (2003) provides a method for mechanizing trading of breakaway gaps known as the “explosion gap pivot.” Runaway gaps, also known as measuring gaps, occur during a trend, often in the middle of a price run. These gaps are traded in the direction of the gap to profit from the directional trend. According to Bulkowski (2010), an upward runaway gap occurs on average 43% of the distance from the beginning of the trend to the eventual peak, and a runaway gap down occurs at 57% of the distance on average.

However, a third type of gap, the exhaustion gap, occurs at the end of a strong trend; because price may reverse immediately or remain in a congestion area for some time, trading these gaps should be avoided. In hindsight it is easy to recognize an exhaustion gap from the profitable breakaway and runaway gaps, but as they are occurring, the gaps can have similar characteristics. In his book The Master Swing Trader, Alan Farley (2000) extends Edwards and Magee’s discussion of gaps to include a “hole-in-the-wall” strategy. Farley gives extended examples of situations where an exhaustion gap occurs in the opposite direction from what would be expected to occur.

Few of the detailed studies of gaps have systematically considered gaps occurring in the stocks of publicly traded companies. Instead, most have dealt with index futures contracts or tracking stocks such as SPY. For example, Weintraub (2007) claims that the tendency for a gap to be closed is indirectly proportional to the size of the gap; he attempts to distinguish between common gaps and breakaway gaps by considering the magnitude of the gap in the mini index futures contracts. Bukey (2008) studies double gaps, defined as two gaps occurring within ten days of each other, in SPY. He finds that double gaps are unremarkable unless they are divided into two categories: filled and unfilled. If SPY gaps up twice within a 10-day period and the first gap was not filled, the market is more likely to fall the next day and then trade sideways. If the first gap is filled, then the SPY drop is often delayed. Also, if the SPY double gaps down and the first gap was filled, then the market is more likely to rebound within four days.

Figure 1, Gaps, or Windows on a Bar Chart

Data and Methodology

To study more closely the gaps for individual stocks, we consider stocks included in the Russell 3000 between January 1, 2006 and December 31, 2010.[1] During this time period, 20,611 gap ups occurred and 17,435 gap downs occurred. With 1,259 trading days in the sample, this is an average of about 16.4 stocks gapping up and 13.8 stocks gapping down each trading day. Although some days, such as April 1, 2009, which had 375 gap up stocks and February 17, 2009, which had 409 gap down stocks, have a much higher observation of gaps, a typical day is characterized by at least a few gaps. Gap ups occurred on 1153, or 91.6%, of the trading days.

Gap downs occurred on 1033, or 88%, of the days. A gap of one variety or the other occurred on 1164, or 92.5%, of the days. The gapping stocks represented a wide range of companies. One-thousand-one-hundred-and-thirty-three of the stocks in our sample experienced at least one gap up, and 1,135 experienced at least one gap down.

Throughout this study, we use “Day 0” to represent the day a gap occurs. For example, consider a gap up. The day before the gap is Day -1 and the stock’s high on Day -1 is the beginning of the gap. On the next day (Day 0), the stock’s low exceeds the high on Day -1. We base our return calculations from the open at the next day (Day 1) to the close on Day 1 to calculate a 1-day return. To calculate longer returns, the return is calculated from the open at Day 1 to the close on the day of the return length; therefore, a 3-day return is calculated as buying at the open of Day 1 and selling at the close of Day 3.

Results

Gap Ups

Table 1 shows the overall results for trades based on observing gap ups. On Day 1, the day following a gap up, a stock averages a price decline of 0.056%.[2] While following a trading strategy of going long a stock that gaps up one day after the gap is not profitable in our sample, this result must be considered given the overall market backdrop of this time period.

Investing in SPY instead of the gap up stocks presented in Table 1 would have resulted in an average loss of 0.06% on these days. Thus, the stocks that gapped up performed much better the day after the gap than did the average stock in the market. If the gapping stock is held for 5 or 20 days after the gap, on average, the return will be positive and higher than the market return. These results suggest that stocks that gap up do, on average, outperform the market over the next several weeks.

A closer look at the data, however, reveals that these gains come from a subset of the stocks—those that are characterized by a white candle on the gap day (such as Gap A in Figure 1). The results suggest that when a stock gaps up and closes higher than it opens, this upward price trend will continue for the next few trading days, leading to a profitable trading strategy. However, if the price gaps up, but the close is lower than the open, even though the gap remains unfilled, don’t expect the upward price movement to continue. Stocks exhibiting these black candlesticks on the day the gap occurs tend to have negative returns, and underperform the market over the next several days.

Looking at the price movement on the day of the gap appears to help identify profitable trading opportunities. What if this analysis is extended to looking at the price movement the day before the gap occurs? Table 2 presents returns broken down by Day -1 candle color. This table shows that a black candle on Day -1 followed by a white candle on Day 0 is associated with above market returns.

Is gap size important to the trader? A gap simply means that there is a void on the price chart at which no shares traded hands. This void could be very small (a penny) or it could be large (several dollars). Kirkpatrick and Dahlquist (2011) suggest that the size of a gap will be proportional to the strength of the subsequent price move for breakaway gaps. Hartle and Bowman (1990) suggest that relatively small gaps are not significant. In order to see if the size of a gap indicates the significance of the gap, we measure the percentage change in price from the Day -1 high to the Day 0 low. We then took the entire sample of gap sizes and broke them into size quintiles. The 5th quintile is comprised of those stocks with the largest gaps.

Table 3 shows the impact of the gap size (in quintiles) on subsequent returns for gap ups. It appears that larger gaps tend to signal that the stock is making a good upward move that may persist. As can be seen, the returns for those stocks in the 4th quartile in terms of gap size are quite strong, especially when a white candle occurred.

Next we consider the question of “How important is the gap day volume?” Traditional technical analysis theory suggests that breakouts that occur on high volume are meaningful, and Kirkpatrick and Dahlquist (2011) claim that heavy volume usually accompanies upward gaps. Nison (2001) states that high volume increases the importance of a window. Tables 4 and 5 provide results for comparing the volume on the gap day to previous short-term volume (3 days) and long-term volume (30 days) for the stock. Little insight can be gained by the data in Table 4 except for the fact that it appears that stocks that gap up on heavier volume tend to outperform those gapping up on low volume at the 20-day time horizon. Looking at volume relative to average volume over a longer time horizon appears more useful. Table 5 shows that stocks gapping up on volume higher than the 30-day average volume consistently outperform stocks that gap up on lower than average volume.

Table 6 shows the results for gaps occurring above and below the 10-day moving average of price. Gap ups that occur below the 10-day moving average of price have positive market adjusted returns for the one-, three-, five-, and 20-day time periods. This suggests that gaps occurring below a 10-day moving average are breakaway gaps, beginning an upward trend; this is especially true for gaps that have a white candle on the day the gap occurs. Gaps occurring above the 10-day moving average tend to have a below market return, suggesting that these are exhaustion gaps.

Tables 7 and 8 further explore the gap occurrence relative to the moving average by considering longer moving averages. Table 7 shows the returns for gaps based upon whether the gap occurs below or above the 30-day moving average, and Table 8 shows the results using a 90-day moving average. These results reinforce the idea that gaps occurring at relatively lower prices tend to outperform gaps occurring at relatively higher prices, especially at the 1- and 3-day time intervals. However, comparing these results to Table 6 we find that gaps occurring below the 10-day moving average tend to have higher returns than gaps occurring below longer moving averages.

Gap Downs

Table 9 begins the exploration of down gaps. A gap down is a downward move; so, a trend following strategy would suggest going short when a gap down occurs. Table 2 indicates that the day following a gap down, a stock’s price does indeed continue to fall. Not only does the stock price fall, but also the fall is, on average, almost two times greater than the decline in the overall market on those days. This downward movement in stock price tends to continue for the next couple of days, resulting in a three-day market adjusted return that is negative.

These results suggest going short the day after a gap down, whether the candle is black or white, but only for the next few days. The positive 5-day and 20-day price movements for the gap down stocks suggests that the downward stock price movement is short lived, and being long these stocks several days after their gap down is profitable.

Table 10 looks at this trending question a little more closely by considering the color of the candle the day before the gap occurs as well as the day of the gap. These results suggest that the shorting strategy is most profitable when a white candle on Day -1 is followed by a gap down. Surprisingly the strongest downward move occurs when a white candle occurs on Day -1 and Day 0. In this case, a short strategy is profitable out to Day 5.

Next, we consider the impact of size on the profitability of trading a gap down in Table 11. As before, the 5th quintile contains the largest relative gap sizes. These results are a bit perplexing. The fifth quintile gap downs are more likely to persist in downward price movement for the first three days following the gap. Remember, however, that on average that we found that gap downs reverse and should be traded long in the 5- and 20-day trading ranges. This is especially true for stocks making a large downward move on the gap. In fact, we find that the market adjusted 20-day return for being long the stocks in the 5th quintile is over 0.8% and for stocks in the 4th quintile is over 1%.

Turning to the question of the impact of volume associated with down gaps, we see some interesting results in Table 12 and 13. While general opinion has been that volume is important when analyzing gap ups, Pring (1991) and Kirkpatrick and Dahlquist (2011) claim that volume is not an important consideration when considering gap downs. However, above average volume, measured either at the 3-day or 30-day level, for a down gap does seem to be associated with better performance of a short strategy at the one- and three-day trading time frames in our study. What is most striking, however, is the performance of the low volume down gaps. Down gaps that appear on low volume must be watched carefully. While these stocks have negative returns the day after the gap (suggesting a short strategy), they have positive returns in the 3-, 5-, and 20-day time horizons, and, especially at the 20-day time horizon, outperform the market. Down gaps occurring on light volume tend to reverse trend quickly; a long position should be taken in these stocks.

Next we considered whether the gap occurred above or below the moving average of price. Table 14 displays the results for the 10-day moving average. This data highlights the fact that it is generally profitable to go short for one day after a gap down; the stocks that gap down fall more than the market the day after the gap, whether the gap occurs above or below the 10-day moving average. The negative movement of the stock price continues to the 3-day time period, but is greater in absolute value than the fall in the general market only for stocks in which the gap down occurs above the 10-day moving average.

Tables 15 and 16 consider longer moving averages. These two tables suggest that the stocks that are already relatively low in price (trading below their 30-day and 90-day moving averages) are the most profitable stocks to short on a gap down for the one-day and three-day time periods. However, these stocks tend to reverse direction and outperform the market at the five-day and 20-day horizons. Interestingly, stocks that experience a gap down when trading above their 30-day or 90-day moving average tend to outperform the market by over 1.3% over the next 20 days.

Conclusion

It is easy to classify gaps as breakaway, runaway, or exhaustion gaps in hindsight. However, after-the-fact classification is not helpful when trading. By looking at the characteristics of unfilled gaps the day the gap occurs, we attempt to identify profitable trading positions to enter the following day. We determine that white candles on the day of the gap are associated with higher returns. Traders should also look for larger percentage gaps, gaps preceded by a black candle, gaps occurring on above average volume, and gaps occurring below the 10-day moving average of price, as these gaps are associated with above market returns. These findings are consistent with much of traditional technical analysis thought.

However, when we turn to gap downs, we find some results that are somewhat surprising. We find that gap downs tend to be followed by downward price movement only for a few days. By five days after the gap down, these stocks actual outperform the market. This is especially true for the stocks that gap down by the largest percentage. Also, stocks that gap down at above average prices are the stocks that tend to outperform the market over the next several weeks. These results suggest that down gaps may be traded in the direction of the trend (that is shorted) for a few days, but that these stocks, especially those with a large gap occurring above the average price and on low volume, are stocks to take a long position in several days after the gap.

Footnotes

- To be included in this sample, a stock had to have a trading volume of over 1 million shares on the gap day and the four prior trading days to ensure that decent liquidity existed.

- Numbers in all tables throughout the paper are percentage returns. Thus “-0.056” in the table represents a 0.056% decline.

References

Bukey, David, “Double Gaps,” Active Trader, Vol. 9 (3), 2008, pp 14-20.

Bulkowski, Thomas N., “Bulkowski’s Free Pattern Research,” http://www.thepatternsite.com, 2010.

Edwards, Robert D. and John Magee, Technical Analysis of Stock Trends, Springfield, MA: John Magee, 1966.

Farley, Alan, The Master Swing Trader: Tools and Techniques to Profit from Outstanding Short-Term Trading Opportunities, New York: McGraw Hill, 2000.

Hartle, Thom and Melanie F. Bowman, “Gaps,” Technical Analysis of Stocks and Commodities, Vol. 8 (12), 1990, pp 453-455.

Kirkpatrick, Charles D. and Julie R. Dahlquist, Technical Analysis: The Complete Resource for Financial Market Technicians, Upper Saddle River, NJ: Pearson Education, Inc., 2011.

Landry, David, Dave Landry’s 10 Best Swing Trading Patterns and Strategies, Los Angeles, CA: M. Gordon Publishing Group, 2003.

Nison, Steve, Japanese Candlestick Charting Techniques, 2nd ed., New York: New York Institute of Finance, 2001.

Pring, Martin J., Technical Analysis Explained, 3rd ed., New York: McGraw Hill, Inc., 1991

Weintraub, Neil, Tricks of the Active Trader: An Insider’s Techniques for Getting the Edge, New York: McGraw Hill, 2007.

A Momentum Trading Effect in Real Estate Funds

by Greg Kuhlemeyer, Ph.D.

About the Author | Greg Kuhlemeyer, Ph.D.

Bio Coming

by Robert Kunkel, Ph.D.

About the Author | Robert Kunkel, Ph.D.

Bio Coming

Abstract

This study evaluates whether there is a momentum trading effect in real estate funds by examining the TIAA Real Estate Account. We employ three return moving averages to develop a technical signal to identify: (i) momentum trading days when investors are invested in the real estate fund and (ii) non-momentum trading days when investors are not invested in the real estate fund. Our tests show a strong momentum trading effect where the mean daily return for momentum trading days is 0.269% and significantly greater than the -0.465% mean daily return for non-momentum trading days. Conversely, when equities and bonds are tested, we find no momentum trading effect. We believe the momentum trading effect in the real estate fund is a function of its underlying assets of real estate properties. The market values of the properties are determined at four discrete times a year by independent third party appraisers rather than daily market prices. Because the underlying assets, real estate properties, are reevaluated much more slowly than publicly traded stocks and bonds, the real estate fund is able to generate momentum trading benefits.

Momentum trading is typically perceived and based on price movements where the goal becomes “buy and sell higher” versus the traditional investment adage of “buy low and sell high”. Stocks with momentum are expected to exceed their moving averages and this is most commonly interpreted, in the most basic design, as a “buy” signal. Momentum investors use a variety of different technical analysis measures for moving averages based on their perception of the correct approach for the situation. There are two concerns with price moving averages. The first concern is that price moving averages are not directly related to returns. This study takes on a unique approach in the literature by utilizing return moving averages that more closely align with traditional fundamentalist views of the risk-return relationship. The second concern is that price, and hence price moving averages, do not convey the same relative information as returns and their associated return moving averages. A narrowly moving stock price can move above or below the price moving average by $1 and it may convey little new information if the stock is trading at $400 or much more if the stock is trading at $4. If any momentum statistic moves either above or below the momentum statistic moving average, then it conveys the relative importance of that day’s new information. In the previous example, clearly a 0.25% move for the $400 stock has much less informational content than a 25% move for the $4 stock. It is this study’s contention that assets with return momentum will signal opportunities to generate returns that will exceed a buy-and-hold strategy. The ability to find a momentum trading effect in a real estate fund would also reject the Efficient Markets Hypothesis (Fama 1970).

I. Literature

Technical and fundamental analyses have been part of the practitioner environment with fundamental analysis generally supported by scientific modeling. Levy (1967) showed that a portfolio of well-performing stocks with relative price strength would continue to perform well whereas a portfolio of poor-performing stocks would continue to perform poorly. This study showed that technical analysis generated benefits. Fama (1970) helped push technical analysis into the background of the academe with his Efficient Markets Hypothesis in its three forms: weak, semi-strong, and strong. The implication is that if the Efficient Markets Hypothesis holds in all forms, then neither fundamental nor technical analysis is valuable. Yet, there continues to be substantial financial resources that follow and utilize technical analysis techniques.

Fundamental analysis has been well established and formally went mainstream through the text publication on value investing by Graham and Dodd (1934). The timing of this text with the Great Depression led a country hungry to understand the economy to readily accept the model. Gordon and Shapiro (1956) followed the fundamental approach with their dividend discount model. Burton Malkiel (1973) combined the Efficient Markets Hypothesis works with fundamental analysis to show that stocks follow a random walk which implies that investors would be best served to follow a well diversified approach and minimize all costs. Subsequent research followed the Efficient Markets Hypothesis and generally supported Malkiel’s contention that low cost index funds were the best approach for small investors. Brinson, Hood, and Beebower (1995) found that 90 percent of the variation in a portfolio’s performance is explained by asset allocation which supports that markets are generally efficient. However, investors are often irrational so prices may not represent the fundamental underlying value and lead to pricing bubbles. In the 1990s and 2000s the financial markets experienced an Internet bubble and a real estate bubble, respectively. Both bubbles ultimately popped resulting in large price declines in their corresponding asset markets. Technical analysis has not disappeared under this fundamental push, but has actually flourished. The historical notion of human nature is to look for patterns as a means of survival and it naturally evolved into the financial markets. The more modern elements were pushed by Charles Dow through a sequence of editorials whose tenets were later referred to as the Dow Theory and involved a rotational approach to technical analysis. Levy (1967) clearly articulated that technical analysis, via a relative strength model, showed companies with price strength had a tendency to stay strong six months later. While this study was eye-opening, it did not have the traditional statistical analysis commonly utilized in fundamental analysis research. Wilder (1978) and Appel (1979) helped technical analysis flourish through their independent developments of the relative strength index (RSI) and moving average convergence/ divergence indicator (MACD), respectively.

Jegadeesh and Titman (1993) kicked the door of technical analysis wide open from an academic perspective. They broke stocks into deciles based on actual performance during the period. The authors then purchased securities in the best performing decile and shorted the worst performing decile to create a no-cost portfolio. Deciles were created based on the preceding one to four quarters and then evaluated thereafter for one to four quarters over the 1965-1989 period. The authors found that momentum in stocks continued and generated a significantly positive return. The consistency of these findings clearly violates the Efficient Markets Hypothesis, but requires investors to frequently adjust the individual holdings in their portfolios.

Grinblatt, Titman, and Wermers (1995) and Wermers (1999) followed by showing evidence of herding behavior among mutual fund managers as these managers were following their own momentum strategies with the former finding that 77 percent of funds showed momentum behavior in their portfolio selections. Malkiel (2003) demonstrated that individuals are behaviorally drawn to engage in market activities that are performing above average causing stocks to overreact to positive news and to underreact to negative news which generates the momentum. Balsera, Chen, Zheng (2009) found the technical indicator of the moving average fails to outperform a buy-and-hold strategy, but a contrarian approach significantly outperforms the buy-and-hold strategy using the major U.S. indices. Bettman, Sault, and Schultz (2009) combined fundamental and technical analysis to generate stronger explanatory power of the return model through the R-squared measure. Kirkpatrick and Dahlquist (2010) provide a thorough summary and discussion of technical analysis methods including trend analysis along with traditional moving averages upon which many elements of technical analysis utilize.

II. Hypothesis Development

Real estate funds operate much differently than equity funds and bond funds. An equity fund consists of a portfolio of stocks that are generally publicly traded with market values more readily established on a daily basis. However, a real estate fund includes a portfolio of real estate assets, such as shopping malls and office buildings. These individual real estate assets are not highly liquid and their market values are not easily established on a daily basis. For example, real estate assets in the TIAA Real Estate Account are appraised each quarter by independent third party appraisers. Given the large number of real estate assets in the portfolio, appraisals are continually received by the portfolio managers and then used to help determine the overall portfolio value and the daily unit value of the TIAA Real Estate Account.

We expect to find a momentum trading effect in real estate funds because the underlying assets, real estate properties, are repriced only four discrete times each year. When the real estate market experiences a downturn or upturn, this will be reflected in the quarterly appraisals. Assume the real estate fund holds 100 real estate properties and real estate prices have declined. Assuming around 50 business trading days per quarter, the manager would be reviewing on average two appraisals per day. If we see a consistent directional change in 34 valuations the first month, then we would reasonably expect the remaining 66 appraisals will follow in the same general direction. In a significant real estate market decline, the first appraisals received will show significantly lower market valuations and result in return declines. While the manager may be expecting the subsequent appraisals to also show lower market values, the manager must wait for the appraisals before the fund’s market value is adjusted. The critical point here is that there must be sufficient information flowing out over a period of time to really assess if the information contained in the returns is really fundamentally a longer-term directional change. More fundamentally, leased space will not be coming up for renewal or adjustment quickly. As such, it may take several appraisals before the market value reaches a new equilibrium. Six months represents all of the assets having gone through two appraisal cycles. This period is sufficiently long enough to represent a short-term change, but also to indicate a more fundamental reevaluation of the underlying assets in the real estate markets.

Meanwhile, the return moving averages will show a momentum trading effect so the investor will move out of the declining real estate fund before all of the information has been captured by the property appraisals in their valuation estimates and subsequently on the fund value. Likewise, when real estate prices rebound the return moving averages will show a momentum trading effect so the investor will move into the real estate fund before all the appraisals have been received and the price increased. The challenge is determining when to switch back and forth with a mechanism that does not create excessive trading. Many investment funds will limit “trading” or movement between their funds. For example, the TIAA Real Estate Account limits exchanges out of the account to once per quarter. While we expect to find a momentum trading effect in real estate funds, we do not expect to find a momentum trading effect in equity funds and bond funds because the market values of the underlying assets, stocks and bonds, are generally established daily.

III. Data and Methodology

The nature of many technical analysis studies have shown that technical trading rules effectively generate returns when transaction costs are excluded, but are ineffective when transaction costs are included. Our objective is to determine if it is possible to identify a momentum trading effect that can be used to outperform a traditional buy-and-hold approach without engaging in excessive trading, without generating direct trading costs, and limiting indirect trading costs. As such, our objective is to be invested when a market is generally moving higher with strong return momentum and staying in a safer cash (money market) account if the market is showing negative return momentum. This methodology might be considered longer-term by those technicians employing intra-day trading methodologies.

A. Data

We utilize a specific category of fund management through TIAA-CREF variable annuity accounts. Our data includes a real estate account, an equity index account, a bond market account, and a money market account. Table I provides a summary of the accounts and their inception dates, asset sizes, expense charges, and investment categories. These accounts are used because they: (i) represent retirement accounts via variable annuities which should reduce trading by the fund; (ii) represent a selection of fund options in traditional investment plans; and (iii) allow investors to move funds between the accounts with some limitations.1 We obtain daily data for January 1, 1992 (or inception date) to September 15, 2010 from TIAA-CREF’s website, http://www.tiaa-cref.org/public/performance/retirement/data/index.html.

B. Moving Averages

While previous researchers have used many moving average lengths, most moving averages have fallen in the 5-day to 180-day range with a variety of weighting methodologies from equally to exponentially weighted. We use three unique return moving averages of 5-, 30-, and 180-days. The 5-day window gives us roughly a one week window into the very short-term momentum of the fund; the intermediate length 30-day return moving average represents a one month window that captures a longer directional trend; and the 180-day period captures two full appraisal cycles and is analogous to Levy’s (1967) 26-week period. Following Balsara, Chen, Zheng (2009) we use the longer 180-day return moving average to capture long-term information and informational content similar to a quarterly moving average, but believe that the short and intermediate terms also convey information that can be readily captured in the period return moving averages.

Daily returns for each calendar day were calculated from TIAA’s daily unit prices with non-trading day unit prices set equal to the last trading day’s unit price. To generate moving averages, we calculate the geometric mean daily return for 5 calendar days (5GR), 30 calendar days (30GR), and 180 calendar days (180GR).

We then create a historical benchmark comparison utilizing 1,300 calendar days or approximately 43 months. The period length is long enough to generate a benchmark that would change very slowly and would match a typical business cycle. Watson (1994) indicates that postwar business cycles have averaged just less than 50 months versus slightly more than the average prewar business cycle of 25 months. Our period of 43 months was chosen as an approximate interim length leaning slightly towards recent trends. In addition, this 3 ½-year window provides a strong baseline moving average estimate that is not overly influenced by shorter informational impacts and reduce trading. We then calculate return moving averages for 5 days, 30 days and 180 days as follows:

![]()

Where 5MA is the 5-day return moving average and 5GRt is the geometric mean daily return for 5 days.

![]()

Where 30MA is the 30-day return moving average and 30GRt is the geometric mean daily return for 30 days.

![]()

Where 180MA is the 180-day return moving average and 180GRt is the geometric mean daily return for 180 days. The result of this approach is that it takes 181 closing prices to generate the first 180GR and 1,300 calculations of the 180GR before we can compute the 180MA statistic. Thus, 1,480 days are needed to compute the 180MA.

C. Momentum Statistics

We create momentum statistics by comparing the geometric mean daily return to the return moving average as follows:

![]()

Where MS5 is the 5-day momentum statistic with a value of one when the geometric mean daily return for the past 5 days (5GR) is greater than the 5-day return moving average (5MA), and otherwise the value is zero. A positive indicator on the real estate account, for example, implies that the real estate fund is seeing acceleration in the positive information from the appraisals of the underlying properties. Unfortunately, this is too short to be relied on to make a trading decision when so many more appraisals are forthcoming and the investor is limited in trading activity.

![]()

Where MS30 is the 30-day momentum statistic with a value of one when the geometric mean daily return for the past 30 days (30GR) is greater than the 30-day return moving average (30MA), and otherwise the value is zero. A positive indicator on the real estate account with this statistic indicates that over the past month the appraisals have been coming in at a higher rate than expected with about one-third of appraisals completed. A reasonable person might expect that this trend would continue.

![]()

Where MS180 is the 180-day momentum statistic with a value of one when the geometric mean daily return for the past 180 days (180GR) is greater than the 180-day return moving average (180MA), and otherwise the value is zero. In this situation we have gone through two complete cycles of appraisals within the real estate account. The long-term trend is clearly very positive that appraisals are continuing to represent a return that is above the historical norm.

The sum of the momentum statistics (5-days, 30-days, and 180-days) equals the total momentum statistic as follows:

![]()

Where TMS is the total momentum statistic and may equal values of 3, 2, 1, or 0. When the TMS equals 3, this is an initial BUY signal where the investor would move funds into the corresponding equity, bond, or real estate accounts. When the TMS equals 0, this is an initial SELL signal where the investor would move funds into the money market account. When the TMS equals 1 or 2, this represents a HOLD signal where the investor moves no funds.

Let us briefly think about what a BUY signal means in regards to the real estate account. The investor in this situation is seeing that returns have accelerated above their historical moving average in the short-term, intermediate and longer-terms. The implication is that the information content here is that over the last 6 months the appraisals have been coming in high enough to drive returns above the historical levels. This is occurring over the last month meaning that they have maintained that strength over that period and even the most recent week is above its historical average. An investor in this case is seeing a strong overall signal that utilizing one of the limited numbers of trades within the account is worthwhile at this point with an expected positive impact on the future earning potential for investors. A SELL signal would be the opposite and a HOLD implies we are getting some mixed long-term signals and we should just wait until we get a more definitive direction.

To minimize trading and avoid TIAA penalties for excessive trading, we add a floor metric for each fund. If the fund’s initial purchase price is $100 per unit, then the floor metric begins at $100. The fund’s floor metric is then reset to the new closing price (typically upward by at least 10% when: (i) the TMS reaches another BUY signal and (ii) the fund’s unit price has risen by more than 10%. Thus, the fund’s unit price would need to move significantly to generate a change in the floor metric. When the fund’s unit prices are falling, the floor metric becomes germane in a decision to move out of the fund and into the money market fund. Funds are switched into the money market fund only if: (i) there is a SELL signal and (ii) the fund’s unit price has fallen 10% below the floor metric. If the fund is down only 8% when a sell signal occurs, we will not move into the money market fund even though it may be an early indicator of a downturn. The floor metric is akin to the adage of let your profits run and cut your losses short. This choice of 10% is designed to significantly curtail the BUY and SELL activities. It is entirely reasonable to reduce this if one is willing to move in and out of different real estate accounts depending on the restrictions imposed. Within the constraints of our data set we felt the 10% movement was appropriate to stay with this single real estate account.

D. Momentum Trading Effect

The momentum statistics have been used to determine when investors should move funds into or out of the equity, bond, or real estate accounts. Those days when funds are invested in the money market account are defined as non-momentum trading days. Those days when funds are invested in the equity account, bond account, or real estate account are classified as momentum trading days. We test the hypothesis that the difference between non-momentum trading returns and momentum trading returns is zero by estimating the following regression for the equity account, bond account, and real estate account:

![]()

Where Rt is the return on the account for day t, α is the intercept representing the arithmetic mean return for the non-momentum trading days, β is the difference between the mean return for momentum trading days and mean return for non-momentum trading days, DTMP is a dummy variable (1 = momentum trading day, 0 = non-momentum trading day) and εt is the error term. The F-value tests whether the difference between mean return for momentum trading days and mean return for non-momentum trading days is significantly different from zero.

The intuition behind the regression model is very straight forward. A negative α coefficient would indicate the model has identified non-momentum trading days that, on average, generate a negative return. A significant t-statistic associated with the α coefficient indicates the negative mean return for the non-momentum trading days in the real estate account is significantly different than a mean expected return of zero. A positive β coefficient would indicate the model has identified the real estate account’s momentum trading days generate a greater return than the non-momentum trading days. A significant t-statistic on the β coefficient would indicate the mean return for momentum trading days is significantly greater than the mean return of the nonmomentum trading days. If the F-test is significant, then this indicates the regression model is statistically robust and highly unlikely to have occurred by chance.

IV. Results

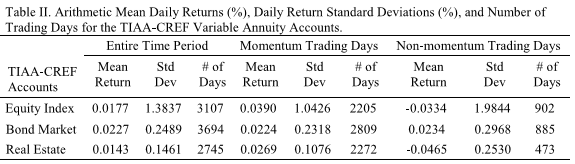

We examine the returns of the Equity Index Account, Bond Market Account, and Real Estate Account. Table II shows the arithmetic mean daily returns and standard deviation for the three TIAA-CREF accounts during the: (i) entire time period, (ii) the momentum trading days, and (iii) the non-momentum trading days. While we find the mean daily returns to be similar for the Equity Index Account and Bond Market Account, we find the mean daily returns to be quite different for the Real Estate Account. More specifically, we find the Real Estate Account has a mean daily return of 0.027% for the momentum trading days versus a -0.046% for the non-momentum trading days. Additionally, we find the Real Estate Account’s momentum trading days not only have a higher mean daily return than the non-momentum trading days, but also a smaller standard deviation at 0.11% versus 0.25% for the non-momentum trading days.

To test for a momentum trading effect, we estimate the regression model in Equation 8 to test whether the difference between mean momentum trading return and mean momentum non-trading return is significantly different from zero. The results of the regression are reported in Table III. When we analyze the Real Estate Account we find a significant difference between the mean daily return for the momentum trading days and non-momentum trading days. We find the difference between the mean daily returns of the momentum trading days and the non-momentum trading days to be 0.073% which is significant at the one percent level. To the average investor, this means that with minimal trading you can increase your daily return by 4.65 basis points by being out of the account when one expects it to decline in value. Over the course of an entire trading year you can improve your performance, on average, by over 2% without incurring any additional trading expenses. Note that our evaluation window covers over a decade and this can have a significant impact on your overall performance as an investor. You may also note that the equity account shows a similar benefit but it is not considered significant. Equities have a much more volatile pricing regime meaning that the returns have a much greater standard deviation, almost eight times greater, and that the result in equities could have reasonably occurred by chance. With the real estate appraisal process the pricing changes occur much slower resulting in a much smaller underlying volatility and making it highly improbable that these results could occur by chance. As such, the regression model clearly shows there is a momentum trading effect in the Real Estate Account. As expected, the Equity Index and Bond Market Accounts show no momentum trading effects as there are no significant differences between the mean daily returns of the momentum and non-momentum trading days. In other words, the β coefficients are not statistically different enough from 0 to be considered significant.

V. Summary Statement

We have developed a technical analysis model which can be applied to real estate funds to create a momentum trading approach that outperforms a traditional buy-and-hold approach. Our model identifies when investors should be invested in real estate funds versus money market funds. We believe the success of momentum trading in real estate funds is a function of the underlying assets of real estate properties, whose market values are not determined daily, but with quarterly appraisals completed by independent third party appraisers. Thus, the need to quickly move in and out real estate accounts is not as critical to investors as it is with stocks and bonds. The technical trading model employs a momentum statistic constructed from three return moving averages along with a floor metric to avoid excessive trading in and out of the funds. Using regression analysis we find a strong momentum trading effect in the real estate fund where the mean daily return using the momentum trading strategy is 0.0734% higher than for the non-momentum trading strategy.

Endnotes

According to the prospectus for the TIAA Real Estate Account, TIAA limits trading to a single move out of the account once per quarter via a telephone conversation with a firm advisor. According to the prospectus for the CREF accounts, with the exception of money market, CREF limits the participants from going out-in-out of the fund within a 60-day window. If the participants violate this restriction, then they are precluded from making moves for 90 days. Note that this excludes transfers via mail. Therefore, mail requests are honored without restriction as indicated above.

References

Appel, Gerald, 1979, The Moving Average Convergence-Divergence Method, Signalert Corporation, Great Neck, NY.

Balsara, Nauzer, Jason Chen, and Lin Zheng, 2009, Profiting From A Contrarian Application of Technical Trading Rules in the U.S. Stock Market, Journal of Asset Management 10, 97-123.

Bettman, Jenni L., Stephen J. Sault, and Emma L. Schultz, 2009, Fundamental and Technical Analysis: Substitutes or Complements?, Accounting and Finance 49, 21-36.

Brinson, Gary P., L. Randolph Hood, and Gilbert L. Beebower, 1995, Determinants of Portfolio Performance, Financial Analysts Journal 51, 133-138.

Fama, Eugene F., 1970, Efficient Capital Markets: A Review of Theory and Empirical Work, Journal of Finance 25, 383-417.

Gordon, Myron J. and Eli Shapiro, 1956, Capital Equipment Analysis: The Required Rate of Profit, Management Science 3, 102-110.

Graham, Benjamin and David L. Dodd, 1934, Security Analysis, McGraw-Hill Book Company, New York, NY.

Grinblatt, Mark, Sheridan Titman, and Russ Wermers, 1995, Momentum Investment Strategies, Portfolio Performance, and Herding: A Study of Mutual Fund Behavior, American Economic Review 85, 1088-1105.

Jegadeesh, Narasimhan and Sheridan Titman, 1993, Returns to Buying Winners and Selling Losers, Journal of Finance 48, 65-91.

Kirkpatrick, Charles. D. and Julie R. Dahlquist, 2010, Technical Analysis: The Complete Resource for Financial Market Technicans, FT Press, Upper Saddle River, NJ.

Levy, Robert A., 1967, Relative Strength as a Criterion for Investment Selection, Journal of Finance 22, 595-610.

Malkiel, Burton G., 1973, A Random Walk Down Wall Street: The Time-tested Strategy for Successful Investing, W.W. Norton, New York, NY.

Malkiel, Burton G., 2003, The Efficient Market Hypothesis and Its Critics, Journal of Economic Perspectives 17, 59-82.

Sortino, Frank A. and Robert van der Meer, 1991, Downside Risk, Journal of Portfolio Management 17, 27-31.

Watson, Mark W., 1994, Business-Cycle Durations and Postwar Stabilization of the U.S. Economy, American Economic Review 84, 24-46.

Wermers, Russ, 1999, Mutual Fund Herding and the Impact on Stock Prices, Journal of Finance 54, 581-622.

Wilder, J. Welles, 1978, New Concepts in Technical Trading Systems, Trend Research, Greensboro, NC.

A Synthesis of Technical Analysis and Fractal Geometry

by Camillo Lento, PhD, CA, CFE

About the Author | Camillo Lento, PhD, CA, CFE

Camillo Lento earned a Ph.D. degree in accounting from the University of Southern Queensland, Queensland, Australia, in 2012. Currently, he is an Assistant Professor of Accounting at the Faculty of Business Administration at Lakehead University, Thunder Bay, Ontario, Canada. Camillo also holds a MSc. and HBComm. Degree, along with being a Chartered Professional Accountant (Canada), a Chartered Accountant (Canada), and a Certified Fraud Examiner.

Abstract

This study develops new insights into the profitability of trading rules through a synthesis of fractal geometry and technical analysis. The Hurst exponent (H) emerged from fractal geometry as a means of detecting longterm dependencies in a time series, the same dependencies that technical analysis should be able to identify and exploit to earn profits. Two tests of this synthesis are conducted. First, financial time series are classified into three groups based on their H to determine if a higher (lower) H results in higher returns to trending (contrarian) trading rules. Second, the relationship between H and profits from technical analysis are estimated through OLS regression. Both tests suggest that the fractal nature of a time series explains a significant portion of the profits from technical analysis.

I. Introduction

Technical analysis is a broad discipline that analyzes past price and volume data to identify patterns that predict future price movements. Identified patterns provide the basis for technical trading rules, which generate buy and sell signals. The efficacy of technical analysis has been researched extensively. The research results are mixed, providing support for (e.g., Brock, Lakonishok and LeBaron (1992), and Gençay (1999)), and against (e.g. Allen and Karjalainen (1999), Lo, Mamaysky and Wang (2000), and Bokhardi et al. (2005)) technical analysis’ ability to forecast security returns.

Recently, Hurst’s exponent (H) (Hurst, 1951) has emerged from fractal geometry into economics research as a means of classifying a time series based on its long-term dependencies (Peters, 1991 and Peters, 1994). A value of H of 0.50 indicates that a series exhibits Brownian motion.[1] 0<H<0.5 indicates an anti-persistent series, suggesting that the data set exhibits mean-reverting tendencies. 0.5<H<1 indicates a persistent series, suggesting the data is trend reinforcing. The strength of the trend increases as H approaches 1. The H thus provides a method of classifying time series, which may be beneficial for the discipline of technical analysis.

The purpose of this study is to develop new insights into the discipline of technical analysis through a synthesis with fractal geometry. The synthesis posits the following: fractal geometry provides a technique (H) that detects long-term dependencies (reinforcing or reverting trends) in the historical price data of a time series; these are the same trends that technical analysis purports to identify and utilize to predict future price movements. Therefore, trending trading rules should be more effective on trend-reinforcing time series, while contrarian trading rules should be more effective in anti-persistent, or mean-reverting, markets.

It is important to note that the discipline of technical analysis includes various technical trading rules. In addition, the technical trading rules can be specified differently, leading to a large number of trading rule variants. Accordingly, popular trending and contrarian rules will be used to test the synthesis. Specifically, trending trading rules will be represented by the filter rule, moving average crossover rule, and the trading range breakout rule, while contrarian trading rules will be represented by the Bollinger Band. In addition, the effectiveness of the technical trading rules is defined as the profits generated from the technical trading rule’s buy and sell signals.

Two empirical tests are conducted to evaluate the synthesis and the resulting relationship between H and profits from technical analysis. First, the financial series are classified into three groups based on their H value (H<0.5; 0.5<H<0.55; H>0.55) to determine if time series having a higher (lower) value H result in higher profits to trending (contrarian) trading rules. Second, OLS regression is used to estimate the relationship between H and profits from trending and contrarian trading rules.

The results suggest that the H is able to identify long-term dependencies in a time series and that these time series result in higher profits to technical trading rules. The classification analysis reveals that profits from trending trading rules are higher (average of 11%) for time series that exhibit long-term dependencies (high H) and lower (average of -16.8%) for time series that exhibit anti-persistent trends. The regression analysis results in a significant R2 of 0.31, revealing that the fractal nature of a time series explains a significant portion of the profits from technical trading rules. The results are consistent with the theory presented by the synthesis.

This study makes a significant contribution to the literature from both a theoretical and empirical perspective as this is the first known study to merge the disciplines of technical analysis and fractal geometry. The extant literature that investigates the fractal nature of financial data seeks only to determine market predictability (e.g. Qian and Rasheed, 2004, Corazza and Malliaris, 2002). This study extends the literature by investigating whether technical trading rules can exploit a time-series’s predictability to generate profits. The results reveal that the fractal nature of a time-series is related to the profitability of different types of trading rules (i.e., trending versus contrarian). Additionally, the results suggests that an investor, who understands the fractal nature of a timeseries, should alter their investment strategy by employing a contrarian trading rule on time-series that exhibits anti-persistence and a trending trading rule on time-series that exhibit long-term dependencies.

The remainder of the paper is organized as follows: Section II provides a review of the literature and develops the synthesis and hypotheses, Section III describes the data, Section IV discusses the methodology, Section V presents the results, and Section VI offers concluding thoughts.

II. Theory and Hypothesis Development

A synthesis of technical analysis and fractal geometry can provide fertile ground for new theory development, along with novel empirical tests, to enhance our understanding of the profitability of technical trading rules. The following literature review develops this synthesis. Section A discusses the technical analysis literature, Section B discusses fractal geometry, and Section C develops the synthesis and Hypotheses.

A.Technical Trading Rules

Early studies on technical analysis conducted by Alexander (1961 and 1964) and Fama and Blume (1966) suggested that excess returns cannot be realized by making investment decisions based on filter rules. However, Sweeney (1988) re-examined the data used by Fama and Blume (1966) and found that filter rules applied to 15 of the 30 Dow Jones stocks earned excess returns over buy-and-hold alternatives. Technical trading rules have also been extensively tested in the foreign exchange market (Dooley and Shafer (1983), Sweeney (1988), and Schulmeister (1988)).

The number of studies on technical trading rules significantly increased during the 1990s. Some of the most influential studies that provide indirect support for trading rules include Jegadeesh and Titman (1993), Blume, Easley, and O’Hara (1994), Chan, Jagadeesh, and Lakonishok (1996), Lo and MacKinlay (1997), Grundy and Martin (1998), and Rouwenhorst (1998). Stronger evidence can be found in the research of Neftci (1991), Neely, Weller, and Dittmar (1997), Chang and Osler (1994), Osler and Chang (1995), Lo and MacKinlay (1997), and Neely and Weller (1998). One of the most influential studies on technical analysis is that prepared by Brock, Lakonishok, and LeBaron (1992) who used bootstrapping techniques and two simple, yet popular, trading rules to reveal strong evidence in support of the predictive nature of technical analysis.

However, not all studies support the efficacy of technical analysis. For example, Allen and Karjalainen (1999) found no evidence that the rules were able to earn economically significant excess returns over a buy-and-hold strategy during the period 1970 – 1989. Furthermore, Lo, Mamaysky and Wang (2000) found that certain technical patterns can provide information when applied to a large number of stocks; however, the results do not imply that technical analysis can be used to generate excess trading profits. Finally, Bokhardi et al. (2005) investigated the effectiveness of simple trading rules and concluded that trading rules cannot be used profitably after adjusting for transaction costs.

B. Fractal Geometry

Fractal geometry has recently emerged into the world of mathematics as a complement to Euclidean geometry as an attempt to better explain and describe the objects and shapes of the real world. In the 1960s, Benoit Mandelbrot believed that Brownian motion[2] was not an adequate statistical description of the true stochastic process generating securities returns. To resolve this inadequacy, Mandelbrot worked in two perpendicular directions. One direction involved relaxing a Brownian motion assumption of finite variance, which introduces what Mandelbrot termed the “Noah Effect.” The other direction entailed relaxing an independence assumption, thereby allowing for a “Joseph Effect.” (Mandelbrot, 1972). The Noah Effect (recalling the Biblical account of the great deluge) refers to the tendency of various time series with presumably independent increments, especially speculative time series, to exhibit abrupt and discontinuous changes.

The Joseph Effect is named after the biblical story in which Joseph prophesied that the residents of Egypt would face seven years of feast followed by seven years of famine (Mandelbrot, 2004)[3]. The Joseph effect denotes the property of certain time series exhibiting persistent behavior (such as years of flooding followed by years of drought along the Nile River basin) more frequently than would be expected if the series were completely random but without exhibiting any significant short-term (Markovian) dependence. To describe such processes, Mandelbrot broadened the idea of Brownian motion into the class of stochastic processes called “fractional” Brownian motion (fBm).

A fractal time series is statistically self-similar regardless of the time frame over which the increments of the series are observed, aside from its scale. For example, a time series of daily, weekly, monthly, or yearly observations would exhibit similar statistical characteristics. Schroeder (1991) notes that the paradigm of random fractals can be described as Brownian motion, that is, a white-noise process, that exhibits these scaling time-series properties.

Fractional Brownian motions exhibit complicated long-term dependencies that can be characterized by the Hurst exponent (H). Mandelbrot developed a statistical technique called rescaled range analysis to measure the Hurst exponent, which generally ranges from 0 to 1 (Hurst et al., 1965)[4]. If 0.5<H<1, the series will exhibit persistence, with fewer reversals and longer trends than the increments of Brownian motion. In this case, the graph would appear smoother than that of a random walk. On the other hand, if 0<H<0.5, then the series will exhibit anti-persistence, as evidenced by a greater number of reversals and fewer and shorter trends than in a white-noise series.

The vast majority of the research that investigates the Hurst exponent in financial market seeks to determine whether H can identify the predictability of the financial market (e.g., Corazza and Malliaris (2002) and Glenn (2007)). For example, Greene and Fielitz (1977) used the rescaled range analysis and found considerable evidence of temporal dependence in daily stock returns for the period December 23, 1963 to November 29, 1968, after accounting for short-term linear dependencies (autocorrelation) within the data. The most popular example is by Peters (1991), who estimates the Hurst exponent to be 0.778 for monthly returns on the S&P 500 from January 1950 to July 1988.

More recently, research has shifted to using the H as part of an investment strategy. For example, Hodges (2006) and Bender et al. (2006) began investigating the possibility of developing portfolios based on identifiable long-term dependencies. Hodges (2006) examined an investor’s ability to form arbitrage portfolios under realistic transactions costs for values of H very different from 0.5. Bender et al. (2006) seeked to develop a general theory of arbitrage portfolio building based on long-term dependent processes. However, neither of these papers specifically focused on investigating the efficacy of technical analysis in light of long-term dependencies.

The research on the H in financial settings has yet to incorporate any elements from the discipline of technical analysis. Specifically, the current body of literature does not use technical analysis to build on the identification of financial market predictability to determine whether profits can be generated after accounting for transaction costs.

C. A Synthesis of Technical Analysis and Fractal Geometry

The extant body of literature provides inconclusive evidence on the profitability of technical trading rules. Furthermore, the literature on the fractal nature of financial markets appears to stop once dependencies have been identified or refuted. New insights into technical analysis can be obtained by extending the literature through a synthesis of fractal geometry and technical analysis.

Technical trading rules are based on the premise that time series exhibit certain patterns in their past data that can be used to predict future movements. It can therefore be deduced that trending technical trading rules (e.g., filter rule, break-out, and moving average rules) should be more profitable on time series that exhibit long-term dependencies. Conversely, time series that are anti-persistent should not provide returns to trending trading rules, as there are no continuing patterns in the time series to identify and exploit. The H can be used to identify the dynamic processes of a time series. Therefore, based on this synthesis, identifying the dependencies in a time-series’ motion should be able to partially explain the inconsistent and conflicting results evident in the extant body of literature. The synthesis of fractal geometry and technical analysis provides the first hypothesis:

H1: The profitability of trending technical trading rules should be higher with time series that have higher Hurst exponents and lower with time series that have lower Hurst exponents.

As opposed to trending technical trading rules, investors may employ a contrarian trading rule. A contrarian rule attempts to exploit a reversal pattern in a time series and essentially sells into strength (expectation of price decline after an increase) and buys into weakness (expectation of a price increase after a decrease). It can therefore be deduced that contrarian technical trading rules should be more profitable on time series that exhibit anti-persistence. Conversely, time series that are persistent should not provide as profitable results as those brought by contrarian technical trading rules, as there are no continuing reversal patterns in the time series to identify and exploit. This reasoning leads to the second hypothesis:

H2: The profitability of contrarian trading rules should be higher with time series that have lower Hurst exponents and lower with time series that have higher Hurst exponents.

Hypotheses 1 and 2 investigate the relationship between H and the profits from trending and contrarian technical trading rules; however, accepting the hypotheses does not suggest that investors can successfully utilize technical analysis to earn abnormal profits by understanding the fractal nature of a time-series because both H and profits will be calculated on the same dataset. Therefore, an additional hypothesis, with a different test, is required to understand whether traders can successfully employ a trading strategy that uses an observed H to correctly employ a trading rule.

H3: The lagged H (Ht-1) can predict whether a contrarian or trending trading rule will be profitable for a time series.

Testing the first three hypotheses will make a significant contribution, as there are no other known studies that test the relationship between profits from technical analysis and long-term dependencies.

Aside from the main hypotheses, an ancillary hypothesis will be tested. Recall that a fractal characteristic is that it should be statistically self-similar regardless of the time frame over which the increments of the series are observed. There is very little empirical evidence on the effectiveness of the trading rules at various scales (e.g., daily, weekly, monthly). Brownian motion suggests that independent increments are identically normally distributed, whereas pure fractal Brownian motion suggests that a time series is statistically “self-similar” (apart from scale) regardless of the time frame over which the increments of the series are observed. There is a vast amount of literature that discusses the non-normality and lack of Brownian motion of stock returns (Cootner 1964, Fama 1965, Officer 1972). If the stock returns exhibit the characteristics of a fractal time series, rather than Brownian motion, there should be no difference in the effectiveness of technical trading rules with data at different scales. This leads to the development of the fourth hypothesis:

H4: There is no difference between the profitability of technical trading rules on the same data set when calculated for different time scales.

III. The Data

H and the profits from the trading rules are calculated for all 30 DJIA stocks (as of July 2008) for the 10-year period of July 1998 to July 2008. The time period was selected as it provides enough data to calculate both the H and the technical trading rules and ends just prior to the 2008 credit crisis. As the data set includes many differing events (e.g., Long-Term Capital Management issues and the Asian crisis in the late 90s, dot-com bubble in early 2000s, etc.), sub-period analysis is conducted to determine the sensitivity of the results to the time period selected.

Trading rules can be calculated at various data frequencies. The data frequency selected depends on different factors and preferences. This study utilizes daily and weekly data. Daily data is used because a typical off floor trader will most likely use daily data (Kaastra and Boyd, 1996). Furthermore, intraday time series can be extremely noisy. Along these lines, weekly data is also used as it is readily available to all traders.

The use of raw daily price data in the stock market has many problems, as movements are generally nonstationary (Mehta, 1995), which interferes with the estimation of the H. The market-index series are transformed into rates of return to overcome these problems. Given the price level P1, P2, … Pt, the rate of return at time t is transformed by:

![]()

where pt denotes the spot price (stock market indices or the exchange rate). The descriptive statistics for the 30 DJIA components are presented in Table 1.

IV. Methodology

The individual and average profits from 12 trading rules, along with H, are calculated for all 30 stocks. Profitability is defined as the returns from the trading rules less the buy-and-hold strategy returns, adjusted for transaction costs. Therefore, by definition, profits can also be negative.

A.Trading rules

The trending trading rules are the moving-average crossover rule (MACO), the filter rule, and the trading range break-out rule (TRBO). A MACO rule attempts to identify a trend by comparing a short moving average to a long moving average. The MACO generates a buy (sell) signal whenever the short moving average is above (below) the long moving average. This study tests the MACO rule based on the following signals:

where Ri,t is the log return given the short period of S, and Ri,t-1 is the log return over the long period L. The following short-long combinations will be tested: (1, 50), (1, 200) and (5, 150). The same MACO rules were tested in the seminal study by Brock, Lakonishok, and LeBaron (1992).

Filter rules generate signals based on the following logic: buy when the price rises by ƒ percent above the most recent trough and sell when the price falls ƒ percent below its most recent peak. This study tests the filter rule based on three parameters: 1%, 2%, and 5%, which is consistent with many seminal, prior studies (e.g., (e.g., Brock, Lakonishok and LeBaron (1992)).

The TRBO generates a buy signal when the price breaks above the resistance level and a sell signal when the price breaks below the support level. The resistance/support level is defined as the local maximum/minimum. The TRBO rule is examined by calculating the local maximum and minimum based on 50, 150 and 200 days, defined as follows:

where Pt is the stock price at time t. Again, these are the same TRBO rules tested by Brock, Lakonishok, and LeBaron (1992). In order to maintain consistency, all of the contrarian trading rules are defined in the exact same fashion as in Brock, Lakonishok, and LeBaron (1992).

The contrarian trading rule will be represented by a variant of the Bollinger Bands (BB). Bollinger Bands are a tool that can be used in a variety of trading rules, not necessarily contrarian in nature. However, this study will employ a contrarian strategy using Bollinger Bands in an attempt to profit from anti-persistent trends in financial time-series. Bollinger Bands require two parameters: the moving average and the standard deviation. Traditionally a 20-period moving average is used. The BB strategy tested will generate a sell signal when the price of the security exceeds the 20-day moving average plus two standard deviations (i.e., the market is said to be overbought). A buy signal is generated when the price of the security is less than the 20-day moving average minus two standard deviations (i.e., the market is said to be oversold). This strategy is denoted by BB(20, 2). In addition to using the traditional parameters, two variants are tested: BB(30,2) uses a 30-day average to determine whether information from longer time frame can generate more informative signals. BB(20,1) uses the traditional 20-day moving average, but uses only +/-1 to generate signals to determine whether a narrower band can generate more precise signals. These are the same BB parameters tested in prior literature (e.g. Lento, Gradeojevic and Wright, 2007).